Payment gateway integration is the process of connecting a website, mobile app, or ecommerce platform to a system that securely captures, encrypts, and routes customer payment data to a bank or payment network for approval. It's the layer that sits between a customer clicking "pay" and your business actually receiving the funds.

Quick reference

- What this covers: integration types, architecture, mobile-specific rules, costs, compliance, gateway selection

- Typical cost: $20,000 to $100,000 for a market gateway (Stripe, PayPal, Braintree). $100,000 to $300,000+ for a custom build.

- Typical timeline: three to six weeks for a basic single-platform MVP. Two to five months for a full production integration.

- Core compliance: PCI DSS (required for all card processing), PSD2/SCA (EU), AML/KYC (fintech, crypto, and high-volume marketplaces)

Want similar results? → Get a Free Quote

You are one step from completing a purchase. The checkout loads. Then nothing, a spinner, an error, or your preferred payment method is not even listed. Most users do not wait. They leave. That single moment of friction is where businesses silently lose revenue every day, and in almost every case, it traces back to how the payment gateway integration was built.

It is the technical layer that connects your app or website to the systems that actually process payments. It manages the handoff between your user, their bank, and the payment network. According to Statista, the global digital payments market is projected to reach US$46.25 trillion by 2031.

No matter whether you have to create a new product, improve the checkout process using drop-off fixes, create a marketplace, or collaborate with a fintech app development company to create a payments-powered platform, the knowledge of the process is critical for your future success. All the information about Stripe integration can be found in this guide, from integration through integration methods to architecture, technology stack, pricing, and more.

What is Payment Gateway Integration, and Why Does It Affect Revenue?

A payment gateway is software that sits between your app or website and the financial system. When a customer enters card details, the gateway encrypts that data, routes it to a payment processor, communicates with the customer's bank, and returns an approval or decline, usually in under two seconds.

Payment gateway integration is the process of connecting your product to that system. That sounds simple, but it involves several moving parts: a frontend checkout UI, a backend API layer, webhook handlers for asynchronous events, security controls, compliance configuration, and ongoing monitoring. A basic single-platform integration can take three to six weeks. A multi-gateway, multi-region build with subscription billing and custom fraud rules can run two to five months.

According to the Baymard Institute, the average documented cart abandonment rate is 70.22%. Poor payment UX, slow load times, missing payment methods, and confusing error messages are some of the top causes. Every unnecessary step in your checkout costs you a measurable percentage of transactions.

Do You Need a Payment Gateway, or in-app Purchases?

If you're building a mobile app, answer this before anything else: what are you selling?

Digital goods or subscriptions (in-app currency, premium features, subscription content) must go through Apple's and Google's own in-app purchase (IAP) systems, not a third-party gateway. This isn't a preference, it's a store policy. Apple and Google both reject apps that route digital-goods payments around their IAP systems.

Physical goods or services (an e-commerce order, a service booking, a marketplace transaction) are exempt from IAP requirements and should use a third-party gateway like Stripe, PayPal, or Adyen.

Key Business Benefits of Payment Gateway Integration

A well-executed online payment gateway integration not only improves transaction success rates but also enhances customer trust and operational efficiency.

- International scope: Process transactions from over 150 countries in various currencies without setting up any payment gateway from scratch.

- Security and trust: Tokenization and encryption ensure the security of customer data, decreasing the risk of fraud and adding to your reputation.

- Improved conversion: Embedded, single-click, and saved card options help simplify the payment process and decrease cart abandonment.

- Faster settlement: New payment gateways facilitate fast settlement of funds, T+1 or T+2 days after the transaction.

- Analytics and reconciliation: Provide transaction information, chargeback management, and revenue reports.

Payment Infrastructure Isn't the Place for Trial and Error

Even minor issues in payment flows can lead to failed transactions, lost customers, and revenue leakage. Build it right from the start with expert guidance.

What's the Difference Between a Payment Gateway and a Payment Processor?

These terms get used interchangeably, but they refer to different things in the payment stack.

A payment gateway captures and transmits payment data from your product to the payment network. It encrypts and tokenizes card information (tokenization replaces the actual card number with a one-time substitute value, so raw card data never touches your server) so it never appears in your app in raw form.

A payment processor handles communication between the payment network, the card scheme (Visa, Mastercard), and the customer's bank. It authorizes or declines the transaction and manages settlement to your merchant account (the account that temporarily holds transaction funds until they clear).

Services like Stripe and PayPal combine both functions. They act as gateway, processor, and often provide the merchant account too, which is why they're the simplest option for most businesses. Dedicated processors like Adyen and Worldpay give you more control and lower per-transaction costs at scale but require more integration work.

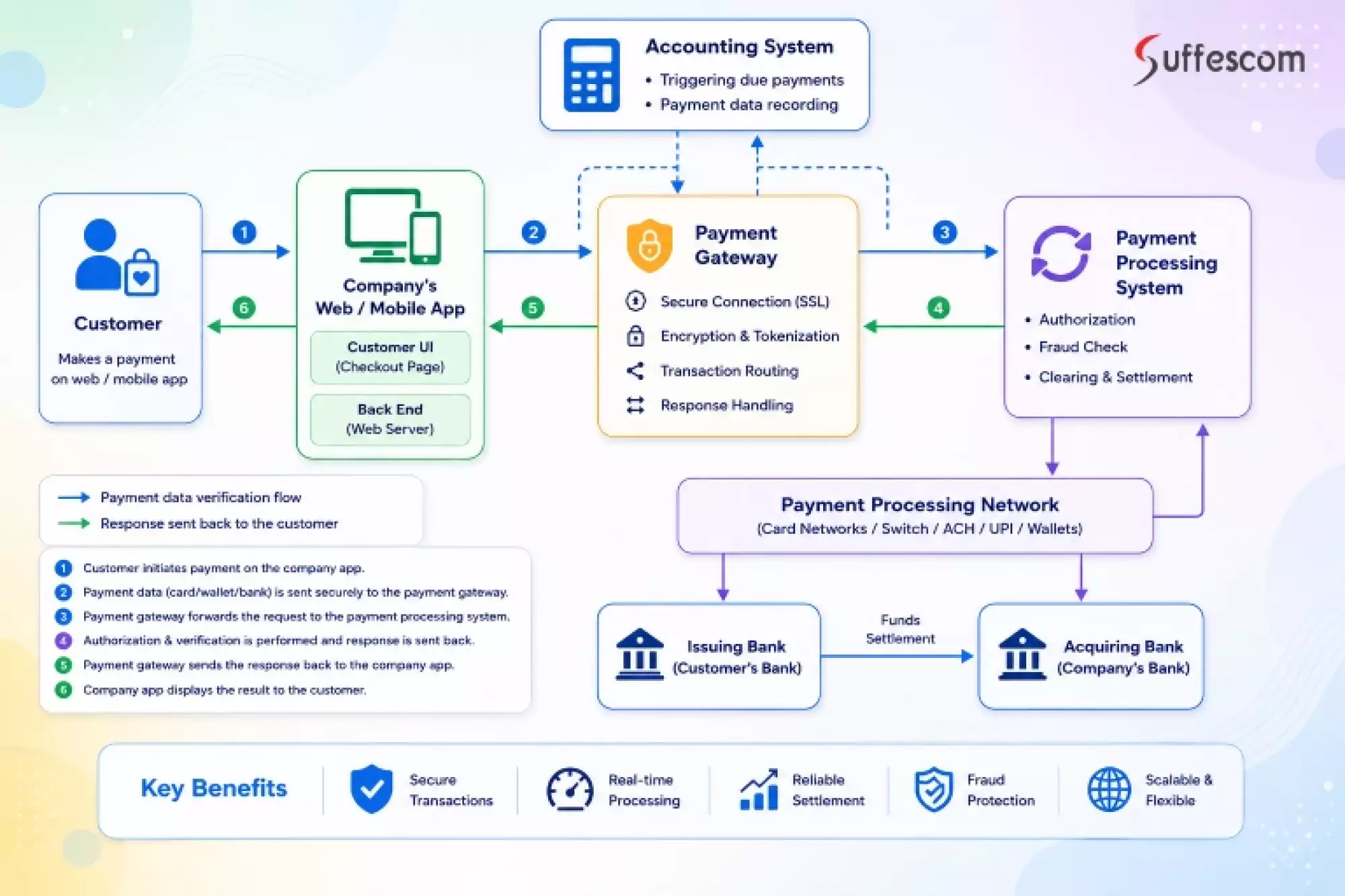

How Does a Payment Gateway Transaction Actually Work?

Understanding the architecture behind payment processing helps developers, product managers, and business owners make smarter integration decisions. Here is what happens between a customer clicking "Pay" and your system registering a successful payment.

Step 1: Customer Initiates Payment

The user enters card details or selects a saved payment method on your checkout page. If you're using the gateway's SDK or JavaScript library, sensitive card data is captured and encrypted client-side; it never reaches your application server.

Step 2: Data is Tokenized and Sent to the Gateway

The gateway library replaces the raw card number with a one-time token. Your backend sends this token along with the amount, currency, and customer metadata to the gateway API over an encrypted HTTPS connection using your secret API key.

Step 3: Gateway Routes to the Payment Processor

The gateway validates the request, applies fraud scoring rules, and routes the authorization request to the payment processor, which forwards it to the relevant card network (Visa, Mastercard, Amex) and then to the customer's issuing bank.

Step 4: Bank Authorises or Declines

The issuing bank verifies funds, checks fraud signals, and may trigger 3D Secure authentication (OTP or biometric). It returns an authorization code or a decline reason. For high-risk transactions, this step adds 0.5–1.5 seconds to the total transaction time.

Step 5: Gateway Returns the Result to Your App

The gateway sends the response back to your application via API response and a webhook event. The API response is synchronous (you get it immediately). The webhook is asynchronous and is the authoritative signal for updating order state.

Step 6: Settlement Arrives in Your Merchant Account

Authorized funds are held by the processor and typically settled to your merchant account within one to three business days (T+1 or T+2), depending on your gateway agreement and processing volume.

Core Participants in the Payment Gateway Transaction Lifecycle

| Stakeholder | Role | Key Responsibility |

| Customer | Initiates payment through a website or mobile application | Completes transactions using cards, UPI, digital wallets, or cryptocurrency |

| Merchant (Business) | Accepts payments and delivers products or services | Integrates payment gateway APIs/SDKs and manages order fulfillment |

| Payment Gateway | Secures, encrypts, and routes payment information | Processes transaction requests and ensures PCI-DSS compliance |

| Payment Processor | Facilitates communication between financial institutions and card networks | Routes payment data through networks such as Visa, Mastercard, and American Express |

| Acquiring Bank | Maintains the merchant account and receives customer payments | Handles fund settlement and transfers payments to the merchant account (typically T+1 to T+2) |

| Issuing Bank | Verifies and authorizes customer transactions | Performs authentication, fraud screening, 3D Secure (3DS) checks, and approval or decline decisions |

How Do You Choose an Integration Approach?

The integration method you choose has the biggest single impact on your PCI compliance scope, development timeline, and how much control you have over the checkout experience. Most businesses settle on one of four approaches.

1. Hosted Payment Gateway (Redirect)

The user is redirected from your website or application to the hosted payment gateway secure page, where payment processing takes place (e.g., PayPal Standard, 2Checkout).

Best suited for: Small businesses, minimum viable product (MVP) releases, and companies lacking technical expertise.

- Lowest PCI scope (SAQ A)

- Fastest to implement — days not weeks

- Gateway handles all security

Drawback: Loss of control over branding; users leave your site/application, higher cart abandonment risk.

2. Embedded iFrame or SDK

Payment fields are embedded in your page via an iFrame or JavaScript widget (e.g., Stripe Elements, Braintree Drop-in UI). Card data is tokenized by the gateway, never by your server.

Best suited for: E-commerce websites and SaaS platforms needing branded payment forms.

- Branded checkout experience

- Moderate PCI scope (SAQ A-EP)

- Well-documented, fast to build

Drawback: Limited customization, requires reliable access to CDN services provided by the payment gateway.

3. Direct API Integration

Your app collects card data and sends it directly to the gateway API. Full control over UI and UX, but you take full responsibility for PCI compliance.

- Complete UI and flow control

- Supports complex payment logic

Drawback: Highest PCI scope (SAQ D), significant security responsibility, much longer build time

4. Mobile SDK integration

Native iOS and Android SDKs from the gateway provider handle tokenization on-device and provide native Apple Pay / Google Pay support.

- Native payment UX on mobile

- Built-in biometric auth support

- Apple Pay and Google Pay included

Drawback: Separate implementation per platform, SDK version management overhead

| Integration Type | Summary |

| Hosted Redirect | Requires the least development effort, minimizes PCI compliance responsibilities, but offers limited control over the checkout experience and branding. |

| iFrame / Embedded | Provides a balanced approach with a smoother user experience while keeping PCI compliance requirements relatively simple. |

| Direct API | Offers complete control over the payment flow, customization, and user experience but comes with the highest PCI compliance and security responsibilities. |

| Mobile SDK | Enables a seamless native mobile payment experience with built-in support for features such as Apple Pay, Google Pay, and mobile wallet payments. |

Architecture: The Three Layers Every Integration Needs

Understanding this architecture helps businesses make informed technical decisions when implementing a payment gateway. It also provides the foundation for scalable payment software development services that support secure transaction processing, settlement management, and payment orchestration.

Layer 1: Frontend — Where the Customer Pays

The checkout UI is what your customer interacts with. In most integrations, this is where the gateway's SDK or JavaScript library lives. The critical principle is this: sensitive card data must never touch your application server. The gateway's client-side library captures the card number, expiry, and CVV, encrypts them, and sends them directly to the gateway's servers, returning a token to your code.

What your frontend is responsible for: displaying accepted card brands, providing real-time field validation, showing a loading state during processing, surfacing clear and actionable error messages, and handling 3D Secure redirects for strong customer authentication.

Layer 2: Backend - Where Payment Logic Lives

Your backend server is where business logic meets the gateway API. It creates payment intents or charge objects, attaches customer data, applies business rules (tax, discounts, split payments), and stores transaction state. Your secret API key lives here; it must never appear in frontend code.

Every payment API call should use an idempotency key. This is a unique identifier that prevents duplicate charges if a network timeout causes a client to retry the same request. Without idempotency keys, a retry storm during an outage can result in customers being charged multiple times — one of the most costly integration mistakes.

Layer 3: Security, Webhooks, and Settlement

Webhooks are asynchronous HTTP requests that the gateway sends to your server when something happens, a payment succeeds, a refund is issued, a dispute is opened, or a subscription renews. This is where most integrations have serious gaps.

The most common webhook mistakes: not verifying webhook signatures (which lets attackers forge payment confirmations), not handling events idempotently (processing the same event twice changes order state), and not building a retry queue for webhook delivery failures.

Integrating a Payment Gateway on a Website: Step by Step

Integration of a payment gateway in website development involves the proper synchronization of frontend UI, backend API logic, webhook implementation, and compliance settings. The following procedure can be applied to the most common web frameworks.

Step 1: Select Your Gateway and Set Up Merchant Credentials

Create an account on the gateway's developer console and complete the KYC/KYB process. This involves providing company documentation and banking information. Retrieve your publishable key (for frontend use), secret key (backend only), and webhook signing secret. Store all keys in environment variables — never in source code.

Timeline: 1–3 days (KYC can take longer for fintech products)

Step 2: Install the gateway SDK

Install the official SDK for your backend language. For the frontend, load the gateway's JavaScript library via a script tag (or the official npm package). Never bundle payment SDKs directly from npm if the gateway provides a CDN-hosted script; the hosted version includes security updates automatically.

- Stripe for Node.js: npm install stripe

- Stripe for Python: pip install stripe

- Razorpay for PHP: composer require razorpay/razorpay

- PayPal for Java: Maven dependency for com.paypal.sdk

Step 3: Create Payment Form / Frontend

If you go for embedding integration, embed the card element from your gateway service into your checkout page. Example for Stripe Elements: Initialize Stripe using your publishable key, create a card element, embed the card element into a DOM node, and listen for PaymentIntent confirmation request upon form submission.

UX Guidelines: show accepted credit card brands' logos, provide real-time validation feedback, show a loading indicator while processing, and show clear error messages like "Your card was declined; please check the number."

Step 4: Server-Side Backend Payment Intent / Charge API Call

Your server creates a PaymentIntent (for Stripe) or an Order (for Razorpay) object prior to user submission of the form. Your server-side call includes amount, currency, customer ID, and any other metadata you want. This stage is often the most critical part of payment gateway API integration services, as it manages transaction authorization, payment validation, and communication between the application and the gateway infrastructure.

Step 5: Configure Webhook Endpoint URLs for Asynchronous Events

These events include payment confirmed, refund initiated, dispute raised, subscription renewals, etc. You register these endpoints on the gateway’s dashboard. Every event should be signed by the gateway so that you can validate signatures against replay attacks.

Step 6: Handle All Possible Payment States

A production integration must handle: Succeeded, Failed, Requires Action (3DS), Requires Payment Method, Cancelled, and Dispute. Map each state to an order status in your database. Never assume success because the user reached a confirmation page, verify through the webhook.

Step 7: Test Everything in Sandbox Mode

You should use the test cards provided by the gateway to simulate all possible situations: a successful charge, card was declined, not enough balance, needs to authenticate via 3DS, network issues, etc. Make sure you automate those in your test suite.

Never skip sandbox testing of failure paths; they're responsible for most production incidents.

Step 8: Go Live & Monitor

Switch API keys from test to live. Set up real-time monitoring for payment success rates, average response times, and error codes. Establish alerts for anomalous failure spikes. Review your first 100 live transactions manually to catch edge cases.

Mobile Payment Gateway Integration (iOS, Android, Flutter)

Mobile app payment gateway integration follows the same architectural principles as web, but with platform-specific implementation details that matter a lot for approval rates, security, and user experience.

iOS Payment Integration

iOS apps use the gateway's native iOS SDK, which handles PCI-compliant tokenization on-device. Stripe's iOS SDK is the most mature, with full support for Apple Pay via the PassKit framework, saved card vaulting, and 3D Secure flows. Integration starts with adding the SDK via Swift Package Manager or CocoaPods, then initializing it with your publishable key in AppDelegate.

Apple Pay is worth implementing from day one; conversion rates on Apple Pay are typically 15–25% higher than manual card entry on iOS, according to Stripe's published benchmarks, because it eliminates the data entry step entirely.

Android Payment Integration

Android integration uses the gateway's Android SDK, added as a Gradle dependency. Google Pay requires registration through the Google Pay Business Console. The critical Android-specific step is checking IsReadyToPayRequest before showing the Google Pay button; not all devices or configurations support it, and showing the button when it's not available creates a confusing dead end for users.

Android-specific: duplicate charge prevention

On Android, the back button can re-fire a payment submit event if the user taps back during processing. Disable the payment button immediately on first submit, use idempotency keys on all API calls, and handle the case where the user returns to the screen after a processing timeout.

Cross-platform: React Native and Flutter

React Native apps use the stripe-react-native package, which wraps the native iOS and Android SDKs and provides access to Apple Pay, Google Pay, and the native card input UI. Flutter apps use flutter_stripe or razorpay_flutter.

Cross-platform SDKs are generally reliable for standard payment flows, but native SDKs are still preferable for complex integrations, particularly where biometric confirmation, deep Apple Pay customization, or specific 3DS handling is required.

Mobile-specific Requirements That Are Easy to Miss

- Deep link handling for 3DS redirects. When 3DS authentication opens a browser, you need a deep link to return the user to your app after authentication. Without this, they're left stranded in the browser.

- Offline state handling. Mobile users lose connectivity. Build a retry queue that stores pending payment requests locally and re-attempts when the connection is restored.

- Certificate pinning. Pinning your TLS certificate prevents man-in-the-middle attacks on payment API calls. This is particularly important for fintech apps handling large transaction values.

- App Store compliance. Apple's rules on in-app purchases apply to digital goods. If your app sells digital content through a payment gateway rather than through Apple's IAP system, it will be rejected. Physical goods and services are exempt.

E-Commerce Payment Gateway Integration

Integration of e-commerce payment gateways has its own distinct demands based on factors such as the amount of the cart, the rate of returns, and the diversity of customer demographics.

| Platform | Integration Method | Key Technical Note |

| WooCommerce | Uses official payment gateway plugins such as WooCommerce, Stripe, and PayPal Payments | Supports extensive customization through PHP filter and action hooks for tailored checkout workflows |

| Shopify | Integrates via Shopify Payments (powered by Stripe) or third-party gateways using the Checkout API | Shopify App Bridge enables embedded payment and merchant experience integrations |

| Magento 2 | Supports native integrations with Braintree and PayPal, along with custom payment modules | Observer events can be used to manage order lifecycle and payment state transitions |

| BigCommerce | Utilizes the Checkout SDK and Payment API for custom payment experiences | Webhooks facilitate automated order fulfillment and payment event handling |

| Custom PHP / Laravel | Direct integration using gateway SDKs and APIs | Laravel Cashier simplifies subscription billing and recurring payment management with Stripe or Paddle |

| Node.js / Next.js | Implements payments using Stripe.js on the frontend and the Stripe Node SDK on the backend | API Routes are commonly used to create and manage Payment Intents securely on the server side |

Payment Capabilities for E-Commerce to Include

- Saved cards/vault: Enable returning shoppers to make payments in just two clicks with tokenized card IDs — no need to store actual card numbers.

- One-page checkout: Do away with checkout processes involving multiple steps; include the payment option directly on the cart page.

- Buy Now Pay Later (BNPL): Incorporate Klarna, Afterpay, or Affirm to boost average cart value and particularly expensive products.

- Dynamic currency conversion: Allow international buyers to pay in their local currencies; boost trust and minimize abandoned carts.

- Abandoned cart recovery: Merge webhook information (payment_intent.created but not succeeded) with email re-engagement workflows.

Choosing the right payment gateway: Stripe vs Adyen vs Braintree vs Razorpay vs PayPal

No single gateway is best for every product. The right choice depends on your target markets, transaction volumes, required payment methods, and technical team capabilities.

| Gateway | Best for | Pricing model | Key strength |

| Stripe | Startups to mid-market, global products | 2.9% + $0.30 per transaction | Best developer docs, 135+ currencies |

| Adyen | Enterprise and high-volume global businesses | Interchange++ (lower at scale) | Best authorization rates globally, own acquiring network |

| Braintree | Marketplaces, subscriptions, PayPal integration | 2.59% + $0.49 per transaction | PayPal vault, strong subscription tooling |

| Razorpay | Indian market, South Asian products | 2% per transaction (domestic) | UPI, net banking, EMI, wallets — all in one |

| PayPal | Global consumer trust, buy-now-pay-later | 3.49% + $0.49 (standard) | Buyer trust in 200+ markets, BNPL via PayLater |

| Authorize.net | US-focused traditional businesses | $25/month + 2.9% + $0.30 | Established US compliance infrastructure |

When to Use Multiple Gateways

Running a single gateway creates a single point of failure. If Stripe has an incident, all your payments fail simultaneously. Larger businesses and platforms often implement a multi-gateway routing layer that sends transactions to the best-performing gateway for each region, card type, or transaction value.

The practical threshold: if your monthly processing volume exceeds $500,000 or if you operate in more than three geographies, a multi-gateway setup is worth the additional integration investment. Below that volume, the operational complexity outweighs the benefit.

What Does Payment Gateway Integration Cost in 2026?

The cost of payment gateway integration depends on factors such as platform type, payment methods, security requirements, and customization needs. Whether you're integrating payments into a website, mobile app, or eCommerce platform, understanding these cost drivers helps you plan a realistic development budget.

| Cost Ranges by Integration Type | Cost Range |

| Single gateway, single platform (hosted/iFrame) — MVP | $5,000 – $20,000 |

| Market-available gateway integration (web + mobile, full production) | $20,000 – $100,000 |

| Multi-gateway integration with routing layer | $60,000 – $200,000 |

| Custom payment gateway — build from scratch | $100,000 – $300,000+ |

| Enterprise-scale with custom acquiring + compliance | $300,000 – $500,000+ |

What Actually Drives Payment Gateway Integration Cost

Businesses that plan to create a payment gateway rather than integrate an existing provider should account for additional costs related to compliance, banking partnerships, payment infrastructure, and ongoing operational management.

| Cost Factor | Lower Cost | Higher Cost |

| Integration method | Hosted redirect or iFrame | Custom direct API with full UI control |

| Number of platforms | Web only | Web + iOS + Android + admin portal |

| Payment methods | Cards only | Cards + wallets + UPI + BNPL + crypto |

| Geographic scope | Single market | Multi-region with local compliance per market |

| Fraud tooling | Gateway defaults (Stripe Radar basic) | Custom ML model + Chainalysis / Kount |

| Recurring billing | None | Subscriptions + proration + dunning + retries |

| Compliance scope | SAQ A (hosted iFrame) | SAQ D + penetration testing + PCI audit |

The Hidden Cost Most Estimates Miss: Post-launch Maintenance

Payment gateways update APIs, deprecate endpoints, and change authentication requirements on a rolling basis. A production integration requires ongoing maintenance, API version updates, compliance re-audits, new payment method additions, and monitoring. Budget 15–20% of your initial integration cost per year for maintenance and evolution. Teams that don't budget for this consistently find their payment infrastructure degrading silently over 12–18 months.

Technology Stack for Payment Gateway Integration in Applications

These are the tools and technologies Suffescom's engineering team relies on across web, mobile, and backend payment projects.

| Layer | Tools / Technologies | |

| Backend | Node.js | Stripe Node SDK, Express, Fastify |

| Python | stripe-python, Django REST, FastAPI | |

| PHP | Razorpay PHP, Stripe PHP, Laravel Cashier | |

| Java / Kotlin | Stripe Java, Braintree Java, Spring Boot | |

| Go | Stripe Go, custom gateway clients | |

| Ruby | stripe-ruby, Active Merchant | |

| Frontend | React / Next.js | @stripe/react-stripe-js, Stripe Elements |

| Vue / Angular | Stripe.js (vanilla), Braintree Drop-in UI | |

| Vanilla JS / jQuery | Stripe.js, PayPal JS SDK, Razorpay Checkout | |

| Mobile | iOS (Swift) | Stripe iOS SDK, Braintree iOS SDK, PassKit |

| Android (Kotlin) | Stripe Android SDK, Braintree Android SDK, Google Pay API | |

| React Native | stripe-react-native, razorpay-react-native | |

| Flutter | flutter_stripe, razorpay_flutter, pay (Google/Apple Pay) | |

| Databases & data storage | PostgreSQL, MySQL, MongoDB | GCP Cloud SQL, Supabase, MongoDB Atlas |

| Cloud infrastructure | AWS, Google Cloud, Azure | EKS, RDS, SQS, Lambda, GKE, Cloud SQL, AKS, Azure SQL |

| Message queuing & event streaming | Apache Kafka | Confluent Cloud, AWS MSK |

| Security & compliance tooling | Sumsub, Onfido | Identity verification, KYC/AML |

| Fraud detection & risk | Stripe Radar | Built into Stripe, configurable rule engine |

| DevOps, containerisation & CI/CD | Docker + Kubernetes | Docker, EKS / GKE / AKS |

| Terraform | Infrastructure as code | |

| GitHub Actions / CircleCI | CI/CD pipelines |

Compliance Requirements You Cannot Skip

Compliance isn't a post-launch checklist item, it's a design decision that has to happen before the architecture is locked in. Retrofitting a payment system to meet PCI DSS requirements it wasn't designed for typically costs three to five times more than building compliance in from day one.

PCI DSS Standards

The Payment Card Industry Data Security Standard governs how card data must be handled. The compliance level depends on your integration method: SAQ A (hosted), SAQ A-EP (iFrame), SAQ D (direct API). Non-compliance results in fines of $5,000–$100,000 per month from card networks.

PSD2 / SCA

The EU Payment Services Directive 2 requires Strong Customer Authentication for online card payments. This means 3D Secure 2.0 or equivalent for EU cardholders. Exemptions exist for low-value (under €30) and low-risk transactions, but the gateway must handle the exemption logic correctly.

GDPR

Any personal data collected during payment — name, email, and billing address — falls under GDPR for EU users. This requires a lawful basis for processing, data minimization, and the ability to delete customer payment data on request. Most gateways handle this at the platform level, but your application's data handling must comply too.

AML and KYC

Anti-Money Laundering and Know Your Customer requirements apply to platforms that facilitate money movement, fintech apps, crypto exchanges, P2P payment platforms, and high-volume marketplaces. This involves identity verification, watchlist screening, transaction monitoring, and Suspicious Activity Report (SAR) filing obligations.

SOC 2 Type II

Enterprise clients, particularly in finance and healthcare, increasingly require their payment service providers to hold SOC 2 Type II certification, which audits security, availability, and confidentiality controls. Not legally required for payment processing itself, but often a commercial requirement for B2B SaaS companies.

3D Secure 2.0

3DS2 is the current standard for cardholder authentication on card-not-present transactions. Unlike its predecessor, it uses a risk-based approach, frictionless authentication for low-risk transactions, and step-up challenges for high-risk ones. It is now required for EU transactions and strongly recommended globally to reduce chargebacks.

Key Considerations for Setting Up an Online Payment Gateway

Before you connect a payment system to your product, slowing down is the right move. The issues that surface in production, such as failed payments, compliance gaps, and poor international coverage, always trace back to decisions skipped at this stage.

| Consideration | Why It Matters |

| Account Type: Dedicated vs Aggregated | Dedicated merchant accounts provide greater control, customization, and lower processing fees at scale. Aggregated accounts such as Stripe and PayPal offer faster onboarding and are well-suited for startups and early-stage businesses. |

| Security and PCI Compliance | Your integration model directly impacts PCI DSS requirements. Using hosted checkout pages, iFrames, or SDK-based integrations can reduce compliance scope, while encryption and tokenization help protect sensitive payment data. |

| Dispute and Chargeback Handling | Effective refund and dispute management processes are essential for maintaining merchant account health. Automated chargeback workflows can reduce operational overhead and improve dispute resolution outcomes. |

| Global and Multi-Currency Support | Businesses serving international customers need multi-currency capabilities, localized payment methods, and payment gateways that support regional transaction processing requirements. |

| Checkout Speed and Reliability | Fast and reliable checkout experiences improve conversion rates and reduce cart abandonment. Performance optimization, CDN utilization, and network testing are critical for maintaining payment success rates. Checkout performance is a major success factor for any e-commerce payment gateway integration, as even small delays can negatively impact conversion rates and customer experience. |

| Payment Method Coverage | Modern customers expect multiple payment options, including cards, digital wallets, UPI, BNPL solutions, bank transfers, and crypto payment gateway integration for greater payment flexibility. |

| Subscription and Recurring Billing | Businesses offering recurring services should implement subscription management features such as automated billing, retry logic, proration, and dunning management to minimize revenue leakage. |

| Fraud Prevention Configuration | Advanced fraud controls such as CVV verification, AVS validation, velocity checks, geo-blocking, risk scoring, and 3D Secure authentication help reduce fraudulent transactions and chargebacks. |

Top Use Cases of Payment Gateway Integration with Real Examples

Payments show up in more places than just a checkout button. Subscription renewals, marketplace seller payouts, in-app purchases, and instant fund transfers each scenario has its own technical requirements and integration patterns. Here is how payment gateway integration looks across the most common product categories:

| Category | Where Payments Apply | Real-World Example | Key Integration Need |

| E-Commerce Platforms | Product purchases and checkout processing | Shopify is integrating Stripe, PayPal, and Klarna | Cart abandonment recovery, saved payment methods, and BNPL support |

| SaaS Products | Recurring subscription and membership payments | Netflix is using multiple payment providers for recurring billing | Subscription management, retry logic, proration, and failed payment recovery |

| Marketplaces | Multi-vendor payments and seller payouts | Etsy facilitates payments between buyers and sellers | Split payments, escrow management, and seller payout automation |

| Fintech and Mobile Banking | Peer-to-peer transfers, bill payments, and card transactions | Revolut's digital banking ecosystem | Real-time payment processing, transaction limits, and biometric authentication |

| Healthcare & Telemedicine | Consultation fees, insurance co-pays, and healthcare payments | Teladoc supports online healthcare transactions | Secure payment processing and healthcare compliance requirements |

| Billing & Invoicing Tools | Invoice payments and recurring billing collections | FreshBooks is offering integrated online payments | Payment links, automated reconciliation, and partial payment support |

| Education Platforms | Course enrollments, subscriptions, and installment payments | Coursera is accepting global payments | Multi-currency support, BNPL options, and regional payment methods |

| Crypto & Web3 Applications | Cryptocurrency purchases, NFT transactions, and digital asset payments | OpenSea is supporting crypto wallet payments | Crypto payment gateway integration, wallet connectivity, and fiat-to-crypto payment support |

Challenges in Payment Gateway Integration and Solutions

The issues in payment integration rarely surface during planning or sandbox testing. They appear when real users start paying, a card declines with no useful message, a payment hangs mid-authorization, or a webhook arrives out of sequence and corrupts an order state. Knowing these challenges ahead of time lets you build defenses into your integration from the start.

1. Payment Failures and Silent Drop-offs

Problem: Vague error messages like 'payment failed' give users no actionable path forward. Many close the app rather than retry. Failure rates spike further when retry logic is missing or poorly configured.

Solution: Implement descriptive error messaging mapped to gateway decline codes. Build smart retry logic for soft declines (insufficient funds, network timeout) while hard-declining cards flagged for fraud. Provide alternative payment method fallbacks at the point of failure.

2. Fraud and Chargeback Exposure

Problem: As transaction volume grows, fraud patterns emerge. Card testing attacks, account takeovers, and friendly fraud chargebacks can accumulate significant losses before being noticed.

Solution: Configure gateway fraud rules from day one: velocity limits, CVV/AVS checks, 3DS2 for high-risk transactions, and geo-blocking for high-fraud regions. For high-volume platforms, integrate dedicated fraud scoring (Stripe Radar, Kount, Sift). Automate chargeback dispute evidence submission to win representments.

3. PCI-DSS and Security Compliance Pressure

Problem: Many teams discover the depth of PCI DSS requirements after already architecting their payment layer incorrectly, having raw card data touch their servers unintentionally.

Solution: Choose your integration type deliberately. Hosted or iFrame integrations keep you at SAQ A or A-EP. If you need direct API control, scope PCI environment carefully, use tokenization throughout, and engage a QSA early.

4. Slow or Stuck Payment States

Problem: A 3-second delay during payment authorization with no feedback makes users assume the transaction failed. They hit the pay button again, creating duplicate charges or abandoned sessions.

Solution: Implement clear loading states and progress indicators from the moment the user submits. Handle payments asynchronously, show a 'payment processing' state, and update via webhook when confirmation arrives. Use idempotency keys on all payment API calls to prevent duplicate charges on retries.

5. Webhook Delivery Failures and Out-of-Order Events

Problem: Webhook events can fail to deliver, arrive out of order, or be replayed. A system that processes a 'payment.succeeded' event after 'refund.created' corrupts the order state.

Solution: Always verify webhook signatures. Design webhook handlers to be idempotent; processing the same event twice should have the same result as processing it once. Store raw event payloads and process them asynchronously via a queue. Implement exponential backoff retry for downstream processing failures.

6. Multiple Currency and Cross-Border Payment Complexity

Problem: International customers face higher decline rates when payments are routed through gateways without strong local acquiring relationships or local payment method support.

Solution: Choose gateways with strong local acquiring in your key markets, or implement multiple gateways to route transactions to the best-performing gateway per region. Support local payment methods (UPI, iDEAL, GrabPay, SEPA) natively rather than forcing international cards on users who prefer local options.

The Next Wave of Payment Gateway Technology

Payment infrastructure is changing faster than most businesses realize. The integrations you build today need to be designed to accommodate the following shifts, either because your customers will expect them or because regulators will require them.

Integration of Tap-To-Pay and NFC Payments

Tap-to-pay or NFC payment solutions are becoming increasingly popular in retail, healthcare services, and other sectors. Payment gateways of the future will have to support both contactless and digital payments via unified payment processing systems.

Replacing One-Time Passcodes with Biometric Authentication

Payment gateway integration will involve replacing one-time passcode authentication with more secure and faster biometric authentication, including facial recognition or fingerprint identification.

Embedded Finance and Super-Apps Ecosystems

The financial services are getting embedded into non-financial apps, offering users such services as payments, lending, and insurance from one ecosystem. This is generating the need for sophisticated APIs and flexible payment infrastructure.

AI-driven Payment Optimization

AI is helping to optimize the payments by improving the authorization rates, reducing payment failures, and detecting any fraud in real-time.

QR Code Payments and Account-to-Account Payments

QR code payments and account-to-account (A2A) payments have become alternative solutions to card-based payments. They operate on the basis of open banking and instant payment ecosystems.

Stablecoin Settlement for Cross-border Payments

Stablecoins (USDC, USDT) are moving from crypto-native products into mainstream payment infrastructure. For cross-border business payments where wire transfers are slow and expensive, stablecoin settlement offers near-instant, low-cost finality. Multiple major payment processors (Stripe, PayPal) have already launched stablecoin payout capabilities. For fintech products serving unbanked markets in Southeast Asia, Africa, and Latin America, this opens up payment rails that were previously inaccessible.

Build a Payment System That Scales With Your Business

From API integrations and compliance to multi-gateway routing, the right implementation can save time, reduce risk, and improve payment success rates.

Begin Your Payment System Integration with Suffescom

A basic setup rarely stays basic for long. As transaction volume grows, so does the list of things a payment system needs to handle correctly: compliance scope, fraud exposure, multi-gateway routing, and the maintenance budget most estimates miss entirely.

As a specialist payment gateway development company with 13+ years of fintech engineering experience, Suffescom has delivered payment integrations across Stripe, Razorpay, PayPal, Adyen, Braintree, and custom crypto gateways for startups, e-commerce platforms, and enterprise clients across 25+ countries.

FAQs

1. What is payment gateway integration?

Payment gateway integration is the process of connecting a website, mobile application, or digital platform with a payment gateway to securely process online transactions through cards, wallets, UPI, bank transfers, and other payment methods.

2. How long does it take to set up a payment gateway?

A standard payment gateway integration takes 2–5 months from requirements analysis to live deployment. A basic Stripe integration on a single platform can take 3–6 weeks. A multi-gateway, multi-region integration with custom compliance requirements typically takes 4–6 months.

3. What is the difference between a payment gateway and a payment processor?

A payment gateway securely captures and transmits payment information, while a payment processor communicates with card networks and banks to authorize and settle transactions.

4. How much does payment gateway integration cost?

Integration of a market-available payment gateway (Stripe, PayPal, Braintree) costs $20,000–$100,000 for a production-grade implementation covering web and mobile platforms. A custom payment gateway built from scratch requires $100,000–$300,000+. A basic single-platform MVP integration can start around $5,000–$15,000.

5. Which payment gateway is best for e-commerce websites?

Popular choices include Stripe, PayPal, Razorpay, Adyen, and Braintree. The best option depends on your target market, transaction volume, supported payment methods, and business requirements.

6. What are the benefits of multiple payment gateway integration?

Multiple payment gateway integration improves payment success rates, reduces downtime risk, supports regional payment preferences, and enables intelligent transaction routing across providers.

7. What security measures should be implemented during the integration of payment gateways?

Businesses should implement tokenization, encryption, 3D Secure authentication, fraud detection rules, webhook signature verification, and secure API key management to protect payment transactions.

8. Can businesses accept cryptocurrency payments through a payment gateway?

Yes. Modern crypto payment gateway integration solutions support cryptocurrencies and stablecoins while allowing businesses to settle funds in either digital assets or fiat currencies.