Developing a payment gateway implies building the technological layer located between the customer performing the payment and the funds going to the merchant’s account: an API-based solution that encrypts card or wallet information, tokenizes it to be PCI DSS compliant, sends it via the acquiring bank and the card network for authorization, and either approves or rejects the payment within 2-3 seconds.

A professional build of such a solution would take 4-12 months depending on the scale, is supposed to be PCI DSS compliant from the very start (not just added later), and will cost you somewhere from $25,000 for an MVP up to $120,000 and above for an enterprise-scale, multi-acquirer solution. The best choice for businesses with high transaction volumes, custom payment logic, or development of the payments as a service offering; not the best option when still trying to validate product-market fit.

Key takeaways:

- A payment gateway is a five-party system: customer, merchant, acquiring bank, card network, issuing bank. Every one of those handoffs happens in under 3 seconds.

- Build vs. integrate is a volume and control decision, not a technology decision. Above roughly $5M in annual transaction volume, custom development typically pays for itself.

- PCI DSS compliance has to be a design constraint from Step 1, not a Step 8 checkbox. Retrofitting it is dramatically more expensive than building it in.

- Total cost realistically ranges from $25,000 (MVP, 4-6 months) to $120,000+ (enterprise, multi-acquirer, 12-18 months).

Who This Guide Is For

This guide is written for the people actually making the build decision, not for the payment processors selling an alternative to it:

- Ecommerce and marketplace platforms wanting to own the checkout experience instead of renting it

- Fintech startups building payments as their core product, not just a feature

- SaaS platforms embedding billing and subscription payments directly into their product

- Banks and NBFCs modernizing legacy payment infrastructure

- Existing gateway operators who've outgrown a white-label solution and need to rebuild at scale

- Crypto and Web3 platforms needing fiat on/off ramps alongside token payments

- Gateway-as-a-service businesses planning to resell payment infrastructure to other merchants

If you're here because your business does none of the above and you just need to accept payments quickly, the honest answer is in the next section: you probably don't need to build one.

What Is a Payment Gateway and Why Does It Matter?

The digital payment industry surpassed $114 billion in 2024 and is projected to reach $361 billion by 2030, growing at over 21% CAGR (Grand View Research). The payment gateway segment specifically is forecast to reach $245 billion by 2033. That growth is the backdrop, not the reason to build. The reason to build is control: over cost, over checkout experience, and over the data a gateway generates.

In essence, it is a virtual connection between five parties at the same time—the consumer, the merchant, the acquirer, the card network (Visa, Mastercard, Rupay, or American Express), and the issuer. Each successful transaction, each completion of an order, each proper handling of a refund, all of it hinges upon the smooth functioning of the gateway.

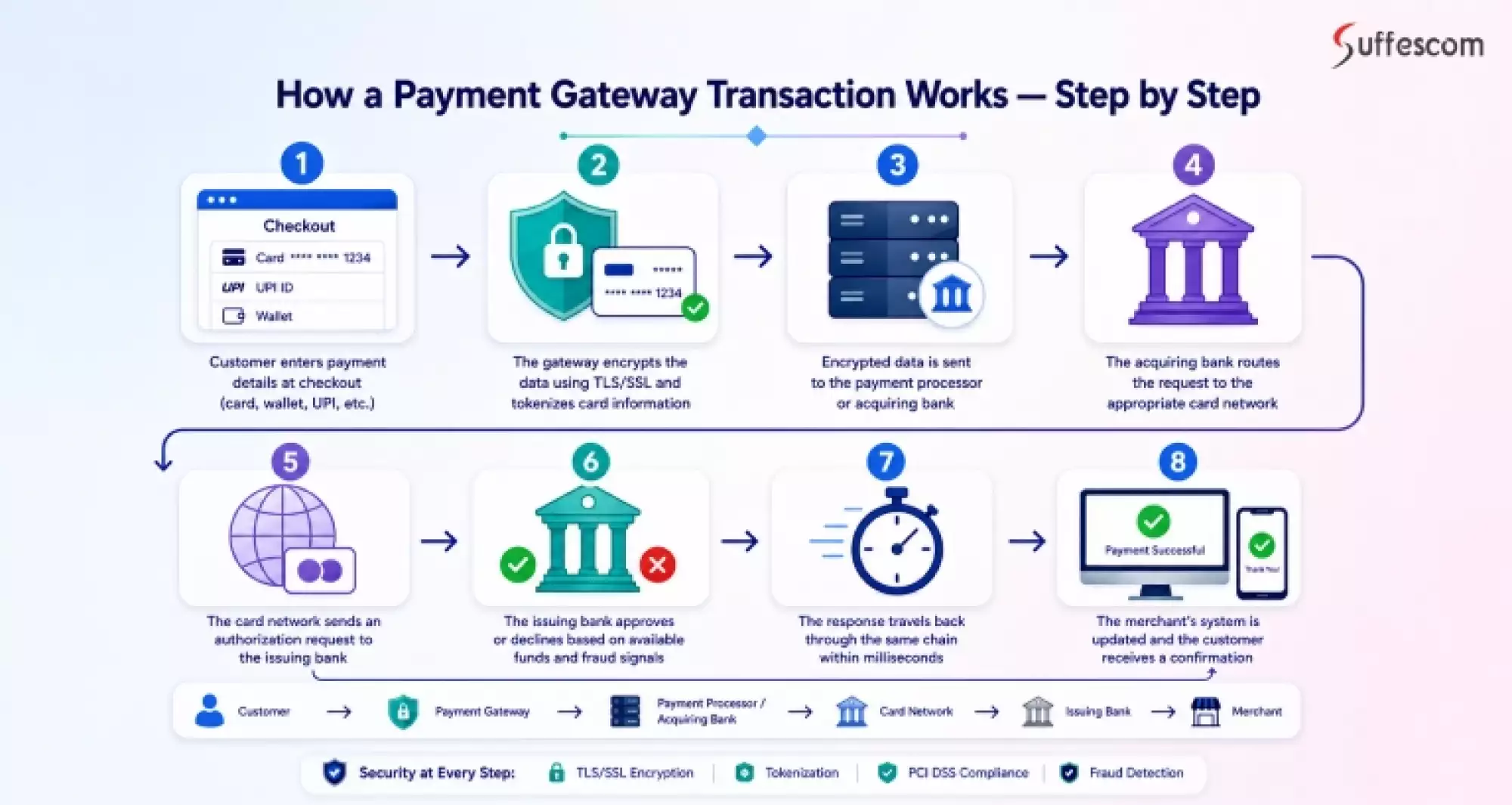

How a Payment Gateway Transaction Works

1. Customer enters payment details at checkout (card, wallet, UPI, BNPL, etc.)

2. The gateway encrypts the data using TLS/SSL (the standard protocol that scrambles data in transit so it can't be read if intercepted) and tokenizes card information (replacing the real card number with a randomly generated substitute that's useless if stolen)

3. Encrypted data is sent to the payment processor or acquiring bank (the bank that holds the merchant's account and receives the funds)

4. The acquiring bank routes the request to the appropriate card network

5. The card network sends an authorization request to the issuing bank (the customer's own bank, the one that issued their card)

6. The issuing bank approves or declines based on available funds and fraud signals

7. The response travels back through the same chain within milliseconds

8. The merchant's system is updated, and the customer receives a confirmation

Planning to Build Your Own Payment Infrastructure?

Partner with a payment gateway software development company that treats compliance as a starting constraint, not an afterthought.

Build vs. Integrate: The Most Important Decision You'll Make

This is the most strategic decision in your payment infrastructure journey. There is no universally correct answer; the right choice depends on your business stage, transaction volumes, technical capabilities, and long-term roadmap.

When building a custom gateway is the right call

- Annual transaction volume exceeds $5 million. At this volume, third-party processing fees become a material cost line. Stripe charges 2.9% + $0.30 per transaction; on $10M in annual volume that's $290,000+ a year, enough to fund significant custom development.

- You need full checkout control for conversion optimization. Baymard Institute data shows 70.19% of shoppers abandon checkout due to friction. A custom gateway lets you design and test every step of that flow.

- Your business model requires custom payment logic, split payments, complex subscription billing, or multi-vendor marketplace settlement

- You operate in regulated markets requiring localized compliance, RBI guidelines in India, PSD2 in Europe, SAMA in Saudi Arabia.

- You're building payments-as-a-product to offer to third-party merchants.

When integrating an existing gateway makes more sense

- You're at MVP stage and need to launch in weeks, not months

- Annual transaction volume is below $2 million; fees are manageable and development cost isn't justified yet

- Your team lacks fintech compliance expertise; PCI DSS and regulatory requirements demand specialized knowledge

- Time-to-market is a critical competitive advantage that can't wait 12+ months

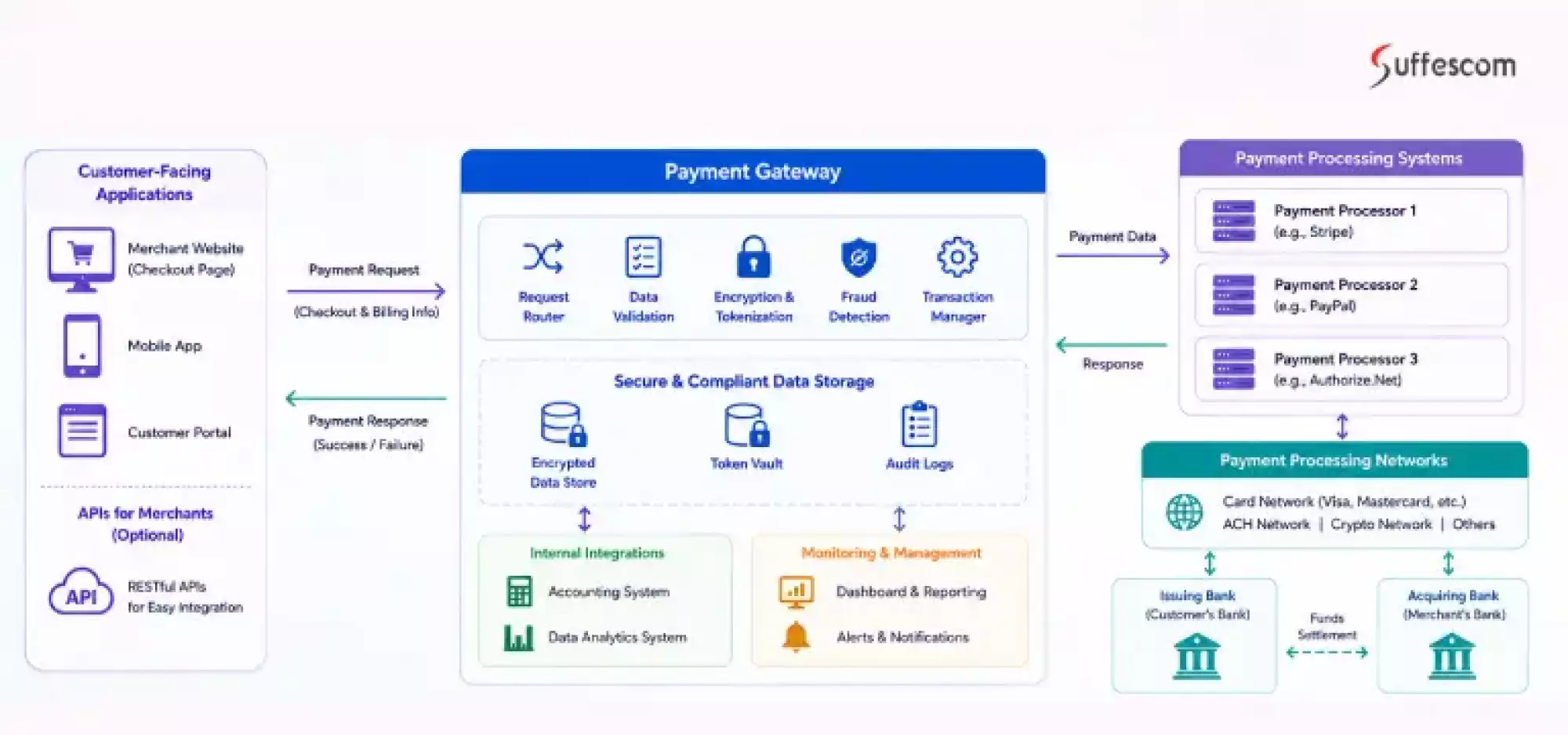

Payment Gateway Architecture: What a Production System Looks Like

A modern payment gateway uses a microservices architecture, meaning each functional component (fraud detection, tokenization, settlement, reporting) is built and deployed independently for resilience and scalability. No single component failure takes down the entire system.

Core architecture layers

API Gateway Tier: Centralized traffic management handling authentication (OAuth 2.0/JWT), rate limiting, versioning, load balancing, and routing for all incoming payment requests.

Transaction Processing Engine: The core authorization layer with high-availability failover, intelligent routing to multiple acquirers, and real-time approval/decline logic.

Tokenization Service: Replaces raw card data with irreversible tokens for PCI DSS compliance and secure card-on-file storage. Sensitive data never exists in raw form within your core infrastructure.

Fraud Detection Module: Configurable rule sets combined with ML-based risk scoring that analyzes transaction patterns, device fingerprints, behavioral signals, and location data in real time.

Payment Processor Adapter Layer: An abstraction layer that standardizes communication with all payment processors (Stripe, Adyen, Razorpay, direct acquirers) so changes to any single processor don't break the system.

Settlement and Reconciliation Engine: Automated processing of refunds, partial refunds, chargebacks, and cross-acquirer reconciliation.

Webhook and Notification System: Real-time transaction event delivery to merchants — approvals, declines, chargebacks, refunds.

Monitoring and Observability: Distributed tracing (Jaeger/Zipkin), APM tools (Datadog, New Relic), TPS and latency dashboards, and automated SLA alerts.

This architecture also supports white-label global gateway deployment, allowing businesses to launch region-ready, multi-branded payment solutions on the same underlying infrastructure.

Features That Make Your Custom Payment Gateway Irreplaceable

Core Features

- Multiple payment methods: cards (Visa, Mastercard, Amex, RuPay), UPI, net banking, digital wallets, BNPL

- Real-time authorization under 3 seconds

- Tokenization and card-on-file for returning customer checkout

- Refund processing: full, partial, and automated reconciliation

- Webhooks for real-time transaction event notifications

- Merchant dashboard with transaction monitoring and reporting

- PCI DSS-compliant data handling throughout

Advanced Features

- Recurring payments and subscription billing for SaaS and membership businesses

- Multi-currency support with real-time FX rates for international merchants

- Split payment and marketplace settlement for multi-vendor platforms

- ML-based fraud detection with configurable risk parameters and adaptive learning

- 3D Secure 2.0 for strong customer authentication with minimal checkout friction

- BNPL integration for higher average order values

- Crypto and stablecoin payment support for web3 merchants

- White-label merchant portal with full branding customization

How To Develop a Payment Gateway: 8-Step Process

Follow a structured approach to develop a payment gateway with the right architecture, integrations, and compliance measures to ensure secure, scalable, and cost-efficient payment gateway development.

Step 1: Discovery, Market Research & Business Planning

Duration: 2-4 weeks

This is the most critical and most underestimated phase. Before a single line of code is written, you need to define:

- Target market and merchant categories you will serve

- Payment methods to support: cards, digital wallets, UPI, BNPL, crypto, bank transfers

- Geographic regions of operation and regional regulatory requirements

- Expected transaction volumes and peak load scenarios

- Whether you will offer gateway services to third-party merchants (gateway-as-a-service model)

- For startups, it is often recommended to begin with an MVP app to validate payment flows before full-scale gateway development.

- Build vs. white-label vs. integrate decision based on budget and timelines

For startups, it's often worth validating payment flows with an MVP before full-scale gateway development. Conduct a thorough competitive analysis and ROI feasibility study here; it's well worth the 2 to 4 weeks it takes.

Step 2: Compliance & Regulatory Framework

Duration: 2-3 weeks (runs in parallel with Step 1)

Compliance is not a post-development checkbox, it's a design constraint that shapes every architecture decision. Building compliance in from the start is dramatically cheaper than retrofitting it later.

Non-negotiable compliance requirements:

- PCI DSS: Any system that stores, processes, or transmits cardholder data. Your compliance level (SAQ vs. full QSA assessment) depends on annual transaction volume.

- 3D Secure 2.0 (3DS2): Strong customer authentication for card-not-present transactions

- AML/KYC: Anti-money laundering and identity verification for merchant onboarding

- GDPR: Data privacy for European customers

- PSD2: Open banking and strong authentication requirements for Europe

- RBI guidelines: India-specific payment processing regulations

- DPDP: India's Digital Personal Data Protection Act

Step 3: Technology Stack Selection

Duration: 1-2 weeks

| Layer | Technologies | Selection Rationale |

| Backend | Node.js, Java, Python, Go | Node.js for high concurrency; Java for stability, Python for fraud ML, Go for high-performance services |

| Frontend | React.js, Angular | Responsive, mobile-first checkout interfaces |

| Database | PostgreSQL, MongoDB, Redis | PostgreSQL for transactional integrity; MongoDB for flexible storage; Redis for caching |

| Cloud | AWS, Google Cloud, Azure | Multi-region deployment, managed services, compliance certifications |

| Security | TLS 1.3, AES-256, HSM, Tokenization | Transport and at-rest encryption, hardware key management |

| Integrations | Visa/Mastercard/RuPay APIs, UPI, Stripe, PayPal | Payment network connectivity |

| Monitoring | ELK Stack, Prometheus, Grafana | Transaction monitoring, SLA tracking, anomaly detection |

| DevOps | Docker, Kubernetes, Jenkins, GitHub Actions | Containerized deployment, CI/CD, horizontal scaling |

Step 4: UI/UX Design: Checkout Experience

Duration: 2-3 weeks

A poorly designed checkout flow directly kills conversion rates. The checkout UI must be intuitive, mobile-responsive, and fast. Design requirements include:

- Minimalist, distraction-free payment form with clear error messaging

- Mobile-first, responsive layout optimized for all screen sizes and browsers

- One-click checkout support for returning customers (tokenized card on file)

- Multi-language and multi-currency support for global merchants

- Accessibility compliance (WCAG 2.1) for inclusive user experiences

Step 5: Core Payment Gateway Software Development

Duration: 4-8 months, the longest and most resource-intensive phase

This is where the actual payment gateway software development happens. Development typically follows a microservices architecture, meaning each functional component, such as fraud detection, tokenization, settlement, and reporting, is built and deployed independently for resilience and scalability.

Key modules developed in this phase:

- Transaction processing engine with high-availability failover

- Card network integration (Visa, Mastercard, RuPay, Amex)

- Tokenization service for secure storage of payment credentials

- Fraud detection module with configurable rule sets and ML risk scoring

- Webhook and notification system for real-time transaction events

- Merchant onboarding and KYC verification workflows

- Reconciliation and settlement automation

- Admin dashboard and reporting interface

This phase is the longest and most resource-intensive, typically spanning 4 to 8 months depending on scope and team size.

Step 6: Security Hardening & Penetration Testing

Duration: 2-4 weeks

Security is not a feature to be added later; it must be validated throughout development and rigorously tested before go-live. Essential security testing includes:

- OWASP Top 10 vulnerability assessment (SQL injection, XSS, CSRF)

- Penetration testing by certified security professionals

- Load and stress testing for peak transaction volumes

- API security testing, such as authentication, rate limiting, and input validation

- Data encryption audit includes TLS configuration, key management, tokenization accuracy

- PCI DSS readiness assessment and gap analysis before certification

Step 7: Banking & Payment Processor Integration

Duration: 3-6 weeks, dependent on bank and network response times

Your payment gateway needs to connect with the financial ecosystem. This requires:

- Acquiring bank partnerships that enable merchant accounts and fund settlement

- Card network certification includes Visa/Mastercard/RuPay connectivity and compliance testing

- Payment processor integrations, where relevant, for routing flexibility

- 3DS authentication server integration for strong customer authentication

- Local payment method integrations such as UPI, NEFT/IMPS for the Indian market; SEPA for Europe; local wallets per market

Step 8: Testing, Sandbox Environment & Deployment

Duration: 2-4 weeks

A robust sandbox environment is mandatory before any live transaction processing:

- Simulate all payment scenarios: successful payments, declined cards, chargebacks, refunds, timeouts

- Test for concurrent transaction processing under expected and peak load

- Validate webhook delivery and notification accuracy

- Perform end-to-end user journey testing across devices and browsers

- Run compliance validation tests for PCI DSS and relevant regional standards

- Conduct final business acceptance testing with representative merchant scenarios

Once all tests pass, deploy to production using a phased rollout strategy, starting with controlled traffic before full go-live.

Ready to Move From Planning to Execution?

Explore our Payment Gateway Development Services to develop a payment gateway tailored to your business model.

Payment Gateway Development Cost: What to Expect

The total payment gateway development cost typically ranges between $25,000 and $120,000+, depending on system complexity, compliance requirements, and scalability needs. The cost of setting up a payment gateway will also be determined by the type of infrastructure used in the construction process, including cloud-based services and security protocols.

| Cost Driver | Why It Matters | Estimated Impact |

| Platform features | Multi-currency, AI fraud detection, dashboards, automation | $20,000–$55,000 |

| Compliance and security | PCI DSS, KYC/AML, encryption, audit logging | $15,000–$40,000 |

| Third-party integrations | Card networks, processors, KYC vendors, banking APIs | $10,000–$35,000 |

| Legacy system connectivity | Middleware and custom APIs for existing infrastructure | $25,000–$60,000 |

| AI and automation | Fraud detection, risk scoring, document verification | $20,000–$50,000 |

| Infrastructure and scalability | Cloud deployment, microservices, API gateways | $15,000–$35,000 |

Timeline by project scope

| Scope | Timeline | Estimated Cost |

| MVP payment gateway | 4–6 months | $25,000–$40,000 |

| Mid-level platform | 6–9 months | $40,000–$75,000 |

| Advanced multi-method gateway | 9–12 months | $75,000–$100,000 |

| Enterprise gateway (multi-acquirer, global) | 12–18 months | $100,000–$120,000+ |

Strategic Reasons to Build a Custom Payment Gateway

Evaluate your business needs carefully to determine when custom payment gateway development delivers the most value in terms of control, scalability, and long-term cost efficiency.

Lower Transaction Fees

Third-party providers like Stripe will charge you 2.9% plus $0.30 for each transaction. In case of an annual transaction flow amounting to $10M+, this is a huge sum of money. With your own custom gateway, you can negotiate with the banks to lower your payments significantly.

Total Brand Control

According to data from Baymard Institute, 70.19% of shoppers leave their cart during checkout due to complicated procedures. Thus, it will be easier for you to design a convenient branded checkout procedure for your consumers.

Improved Security and Anti-Fraud Mechanisms

According to reports from Cybersecurity Ventures, global losses from fraud transactions have reached $48 billion. Custom gateways allow you to implement artificial intelligence-based anti-fraud systems.

Unique Transaction Data

With a custom gateway, transaction data is generated each time you complete a transaction. That information can be leveraged into business insights to drive decisions.

Effortless System Integration

A custom payment gateway integrates seamlessly with existing ERP, CRM, accounting software, and eCommerce platforms. If your goal is to enable secure payment gateway integration in mobile & web apps, a well-designed API architecture simplifies deployment across multiple digital channels.

Global Expansion

Your custom payment gateway will support multiple currencies, local payment systems (UPI, Pix, SEPA), and banking systems.

Common Pain Points in Payment Gateway Development, and How to Solve Them

Developing a payment gateway can be among the most difficult tasks within the realm of fintech software development. Knowing the potential hurdles helps to avoid unpleasant surprises in the middle of the project.

Pain Point 1: Integration With Multiple Payment Processors

As you expand the geographical reach of your payment gateway, you will inevitably need to integrate with several different payment processors. This entails managing API specifications, authentication and security mechanisms, etc. Any changes made to any of those by a third-party provider can cause problems.

Solution: Design a processor abstraction layer that makes communication with all kinds of processors uniform. Establish constant monitoring and keep in touch with processor support teams.

Pain Point 2: PCI DSS Compliance And Its Complexity

Being PCI DSS compliant is a must-have but a difficult task to achieve and maintain. You will have to make a significant amount of preparations, technical changes and undergo regular audits. First-time builders often underestimate what is necessary.

Solution: Consult a Qualified Security Assessor (QSA) early in the development lifecycle to define your compliance scope and requirements. Design your system to minimize PCI DSS exposure by using tokenization, encryption, and secure vaulting, ensuring that sensitive card data is never stored or directly processed within your core infrastructure. Additionally, leverage hosted payment fields or third-party tokenization services where possible to further reduce compliance burden and simplify audits.

Pain Point 3: Fraud on a Larger Scale

Fraud patterns change all the time. A solution that worked against fraudsters last year will likely not work this year. Rules-based fraud detection mechanisms get outdated pretty fast, which causes both fraud and false positives that irritate genuine clients.

Solution: Implement adaptive machine learning-based fraud detection systems. Apply filters based on hard-coded rules for known fraud signatures while using probability-based scoring to address novel attacks. Carefully monitor false-positive ratios, as blocking too many legitimate transactions is just as bad as fraud.

Pain Point 4: Scaling High Availability

Payment gateway systems must be up and running all the time. A 99.9% uptime SLA translates into more than eight hours of downtime per year. This is unacceptable for companies processing millions of transactions daily. To design your system for higher availability, you must make critical decisions about your architecture.

Solution: Design your system for multi-region deployments with automatic failover capabilities. Use circuit breakers between microservices to limit failures. Implement structured logging, TPS, and latency monitoring and real-time alerts on anomalous behavior.

Pain Point 5: Chargeback and Dispute Management

Chargebacks are one of the most frustrating operational problems faced by payment gateway providers. Without adequate tooling, dispute management becomes a manual, error-prone, and expensive process.

Solution: Build an automated dispute management workflow with evidence collection, timeline tracking, and bank communication logging. Integrate with chargeback prevention networks (e.g., Ethoca, Verifi) to resolve disputes before they become formal chargebacks.

The Future of Payment Gateway Development: Trends and Innovations

The payment technology environment is evolving much faster compared to previous years. To develop software products of the future that meet demands in five years ahead, you need to keep up with current payment trends.

AI-powered Fraud Detection: Behavioral Biometrics

Nowadays, machine learning models trained on billion-transaction databases are used for detecting fraud attempts. In the future, gateways will rely on real-time behavioral biometrics and device intelligence for seamless and invisible authentication.

Embedded Finance and Payment Services

Business entities operating in such areas as retail, logistics, healthcare, and SaaS are embedding payment functionality in their services and products. Platforms and gateway-as-a-service (GaaS) solutions are becoming increasingly popular.

Real-time Payment Rails Support

The development of payment instruments such as UPI in India, FedNow in the United States, and open banking in Europe creates expectations related to instant settlements. Accordingly, future gateways must be able to operate under real-time payment infrastructure.

Cryptocurrency and Stablecoin Payments

With growing enterprise adoption of crypto payments and the rise of stablecoins, gateways supporting blockchain-based transactions will serve a rapidly expanding merchant base.

CBDC integration

As central bank digital currencies move from pilot to deployment, payment gateways will need CBDC settlement rails, adding a new integration layer that API-first architectures are better positioned to absorb.

What Makes Suffescom a Reliable Payment Gateway Development Partner

Proven expertise in payment gateway software development, backed by strong capabilities in payment gateway development services for building secure and scalable platforms.

Security-first approach aligned with PCI DSS standards, supported by advanced encryption and tokenization practices, along with experience in blockchain development for enhanced transaction integrity.

Dedicated compliance and risk management frameworks, combined with deep domain knowledge from delivering complex solutions through fintech app development.

Cross-industry experience spanning eCommerce, BFSI, fintech, and on-demand platforms, enabling tailored payment gateway development services.

Agile development approach with rapid onboarding, iterative releases, and continuous integration for faster time-to-market.

Transparent development process with optimized payment gateway development cost and long-term maintainability.

Real-World Implementation: PaylanceX Case Study

PaylanceX

Scaling Global Payments with Custom Gateway Development

A global e-commerce brand partnered with Suffescom for custom payment gateway development to reduce high transaction fees and improve reliability. The solution included multi-acquirer integration, intelligent routing, and PCI DSS-compliant security. As a result, the client reduced processing costs by 30% and increased transaction success rates by 25%, demonstrating the impact of optimized payment gateway development.

View Case Study

FAQs

1. How long does it take to create a payment gateway?

A minimum viable payment gateway takes about 4-6 months. A full-featured, enterprise-level payment gateway with a sophisticated fraud detection system, multi-currency support, and marketplace payment processing capabilities requires up to 12-18 months for development. Time frames depend on several factors, including team size, compliance requirements, and integration capabilities.

2. Is PCI DSS compliance required for a custom payment gateway?

Yes, any organization that stores, processes, or transmits cardholder data should be compliant with PCI DSS standards. Your level of compliance depends on the volume of transactions per year. Engage a qualified security assessor during development to understand your compliance requirements.

3. How much does it cost to build a payment gateway?

The cost of payment gateway development typically ranges from $25,000 to $120,000, depending on complexity, integrations, and compliance requirements. Basic solutions with limited payment methods and features fall on the lower end, while enterprise-grade gateways with multi-acquirer support, advanced fraud detection, and global scalability require higher investment.

4. What is the difference between a custom payment gateway and a white-label solution?

A custom payment gateway is built from scratch, offering full control over features, integrations, and cost optimization. A white-label payment gateway allows faster deployment with pre-built infrastructure but offers limited customization and dependency on the provider.

5. Can a payment gateway support multiple payment methods in one checkout?

Yes. A modern payment gateway can support cards, UPI, net banking, wallets, BNPL, and other options in a single checkout flow. A payment orchestration layer dynamically shows relevant methods based on user location, device, and transaction context, improving conversion rates and reducing drop-offs.

6. How secure is my data when using a payment gateway?

Payment gateways secure data using encryption (TLS 1.2/1.3), tokenization, and PCI DSS compliance. Sensitive card details are never stored in raw form. Additional protections like 3D Secure, fraud detection models, and real-time monitoring help prevent unauthorized transactions and ensure safe processing.

7. What is the distinction between a payment gateway and a payment processor?

A payment gateway is the frontend and merchant portal technology that collects, encrypts, and transfers payment details. A payment processor is the backend technology that communicates with card networks and banks to verify and settle payments. In some cases, the gateway works with several payment processors. When building a payment gateway, you can be the gateway and the processor.