Technology has transformed the microfinance banking software sector from manual ledgers to high-speed digital ecosystems. The surge in microfinance banking software development is driven by the need for automation, AI-based risk assessment, and mobile-first accessibility.

Digital platforms allow institutions to scale rapidly while reducing operational costs. Explore the essentials of microfinance management software, covering critical features, development costs, and the strategic process required to build a competitive fintech product in today’s evolving market.

Build Your Microfinance Software

Validate your idea with expert fintech guidance and planning

Difference Between Traditional Banking Software And Microfinance Management Software Development

While both systems manage money, the core architecture of microfinance management software is built for agility and high-volume, low-value transactions, whereas traditional banking software focuses on complexity and heavy asset management.

| Feature | Traditional Banking Software | Microfinance Management Software |

| Primary Goal | Managing large deposits, mortgages, and corporate wealth | Facilitating financial inclusion and micro-entrepreneurship |

| Credit Scoring | Relies on formal credit bureaus and historical financial data | Uses alternative data (mobile usage, utility bills, social patterns) |

| Transactional Volume | Moderate volume, high-value transactions | Extremely high volume, low-value (micro) transactions |

| Accessibility | Built for branches and formal web portals | Mobile first. Often includes offline modes for rural field agents |

| Interest & Fares | Standardized rates. Monthly/yearly cycles | Flexible, often weekly or bi-weekly repayment schedules. |

| Collateral | Required (Real estate, vehicles, or securities) | Often collateral-free or based on group guarantees (social collateral). |

Key Stakeholders (MFIs, NBFCs, Startups, NGOs)

Understanding the key stakeholders is crucial for microfinance banking software development as each group has distinct operational needs, regulatory hurdles, and user bases.

Whether you are a fintech software development company or a project manager, you must tailor the software architecture to satisfy these four primary pillars:

Microfinance Institutions

These are the software's primary users. Their focus is on operational efficiency and reaching customers at the last mile.

Software Needs

Robust core banking systems, field officer tracking, and automated reporting for donors or central banks.

Pain Point

Transitioning from paper-based systems to digital without losing data integrity.

Neo Banking Financial Companies

NBFCs are profit-oriented entities that provide banking services without holding a full banking license. They are often the most tech-forward stakeholders.

Software Needs

Advanced loan management software development with integrated AI for credit risk assessment and seamless payment gateway integrations.

Pain Point

Scaling rapidly while maintaining a low cost-to-income ratio.

Fintech Startups

Startups like Brigit or EarnIn focus on Neolending. They often target specific niches, such as gig workers or students.

Software Needs

High-performance APIs, mobile-first UX/UI, and real-time earned wage access features.

Pain Points

Customer acquisition costs and navigating complex financial regulations in different jurisdictions.

NGOs & Credit Cooperatives

These organizations often view microfinance as a social mission rather than a high-profit business.

Software Needs

Impact tracking (measuring how much loans improve lives), grant management, and multilingual support for rural users.

Pain Point

Limited budget for high-end custom development, often requiring modular or SaaS based microfinance tools.

Top Player In the Microfinance Banking Sector

The top players in the microfinance and neo-lending space have moved beyond simple banking to become an integrated ecosystem for financial health.

Their dominance is built on a specific technological triad: Alternative Data, Behavioral AI, and embedded financial wellness.

1. Brigit - Predictive Overdraft Logic

Uses agentic AI to predict account depletion before it happens, automatically pushing advances to prevent fees from accruing.

2. EarnIn - Earned Wage Access

Real-time integration with employer payroll systems to allow users to stream their pay as they earn it.

3. MoneyLion - Super App Ecosystem

Combines AI-driven credit building, managed investing, and cash advances into a single high-performance financial hub.

4. Tilt - Non Traditional Underwriting

(Formerly Empower) Analyzes 250+ non-traditional signals (income patterns, utility consistency) instead of FICO scores.

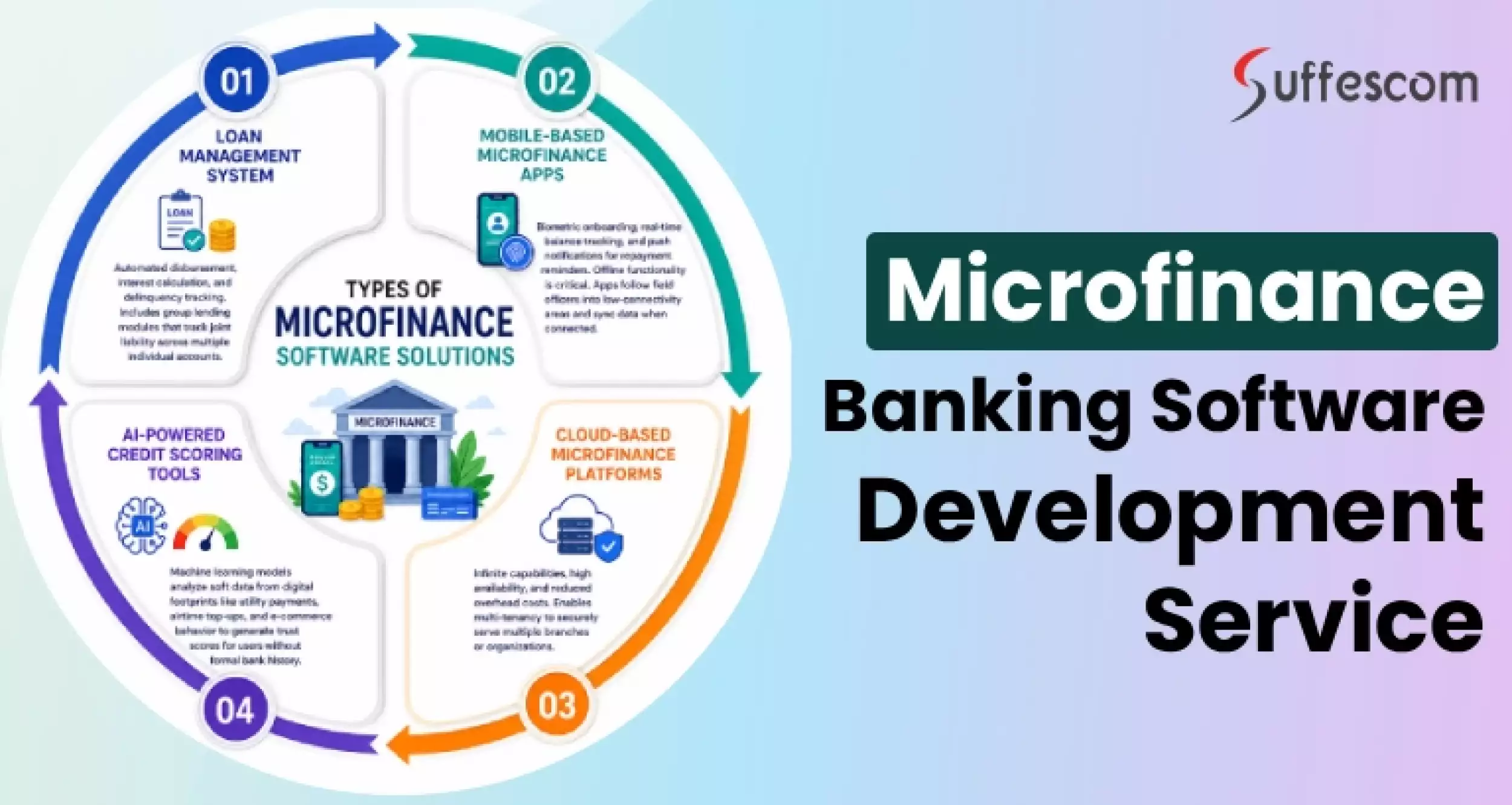

Types of Microfinance Software Solutions

Most modern platforms are a hybrid, but specialized microfinance banking software development typically falls into these four categories:

1. Loan Management System

A specialized LMS handles the complex mathematics of micro-lending that standard banking software often misses.

Automated disbursement, interest calculation, and delinquency tracking. Includes group lending modules that track joint liability across multiple individual accounts.

2. Mobile-Based Microfinance Apps

A complete bank in an app is the primary touchpoint for stakeholders like EarnIn and MoneyLion.

Biometric onboarding, real-time balance tracking, and push notifications for repayment reminders. Offline functionality is critical here. Apps must follow field officers into low-connectivity areas to collect data in sync once they reach a 5G or satellite link.

3. Cloud-Based Microfinance Platforms

Rather than building on-premises servers, most new fintech software development happens in the cloud (AWS, Azure, or Google Cloud).

Infinite capabilities, high availability, and reduced overhead costs. Allows small MFIs to use plug-and-play features. It enables multi-tenancy. One software instance can securely serve multiple branches or even different, smaller organizations.

4. AI-Powered Credit Scoring Tools

Traditional scoring is a barrier to functional inclusion. AI tools are the gatekeepers that make microfinance viable for the unbanked.

Machine learning models that analyze soft data. These tools ingest data from a digital footprint. Utility payments, airtime top-ups, and even e-commerce return rates. Generate a trust score for users without a formal bank history.

Must-Have Features in Microfinance Banking Software

To build a platform that competes with MoneyLion or EarnIn, your feature set must balance rigorous regulatory compliance with a frictionless user experience.

Core Features

Loan Origination & Processing

A digital workflow that captures applications, assigns them to loan officers and manages the approval hierarchy. Must support instant disbursement to linked debit cards.

Customer Onboarding (KYC/AML)

Automated identity verification is essential. This includes OCR for reading government IDs, liveness checks, and real-time screening against global AML watchlists.

Repayment Tracking

A dynamic ledger that handles micro repayments. It must support various interest models — Amortization = (P × r × (1 + r)^n) / ((1 + r)^n − 1)— and provide users with a clear path to zero visual.

Multi-Currency & Multi-Language Support

For MFIs operating across borders (e.g., Sub-Saharan Africa or SE Asia), the software must handle local currency fluctuations and provide localized interfaces to ensure user trust and clarity.

Advanced Features

AI-Based Risk Assessment

Uses machine learning to evaluate thin-file borrowers by analyzing cash flow patterns, utility payments, and behavioral biometrics instead of relying solely on FICO scores.

Mobile Wallet Integration

Direct links with Apple Pay, Google Pay, and regional giants (M-Pesa, GCash) enable one-tap disbursements and repayments, significantly reducing friction and delinquency.

Real-Time Analytics

Institutional: Dashboards for Portfolio at risk and collection efficiency.

End User: Financial health scores and spending insights to improve money management.

Automated Nudges

Employs behavioral economics via SMS/Push notifications. These proactive nudges can improve collection rates by up to 30%.

Build Smart Lending Platform

Launch scalable apps with AI scoring and seamless payment integrations

Microfinance Application Software Development Process

A successful fintech software development company follows this streamlined 7-step lifecycle to ensure security and scalability:

1. Requirement Gathering

Defining project scope, target jurisdiction, and regulatory compliance needs (KYC/AML).

2. Market & Competitor Analysis

Studying leaders like Brigit or MoneyLion to identify unique value propositions and feature gaps.

3. UI/UX Design

Creating high-trust, mobile-first interfaces with intuitive navigation for both borrowers and field agents.

4. Development & Integrations

Building the core engine and connecting essential APIs (payment gateways, open banking, AI scoring). Many businesses also rely on a reliable fintech integration service to securely connect legacy banking systems, mobile wallets, and third-party financial infrastructure.

5. Testing & QA

Rigorous security audits, penetration testing, and stress testing for high-volume microtransactions.

6. Deployment

Phased rollout starting with a Beta/MVP to gather real-user data before a full-scale launch.

7. Maintenance & Upgrades

Continuous monitoring, security patches, and feature updates based on market shifts.

| Layer | Recommended Technology | Reason |

| Frontend (Web) | React.js / Next.js | High-speed rendering and excellent SEO for web portals |

| Mobile (iOS/Android) | Flutter or React Native | Essential for cross-platform efficiency and high-performance UX. |

| Backend Framework | Node.js (Fastify) or Spring Boot | Node.js is perfect for real-time APIs; Spring Boot for enterprise-grade stability. |

| Programming Language | TypeScript / Java / Python | TypeScript prevents runtime errors; Python is the king of AI/ML integration. |

| Database | PostgreSQL (Relational) + MongoDB | PostgreSQL for transaction integrity; MongoDB for flexible user data profiles. |

8. Cloud Infrastructure

Traditional servers are obsolete, utilize cloud native SaaS models:

Hyperscalers

AWS or Google Cloud are preferred for their FinTech-ready compliance templates.

Architecture

Microservices and serverless (using AWS Lambda). This allows you to scale the loan disbursement module independently from the user profile module during peak hours.

Edge Computing

Deploying code at the edge (Cloudflare workers) to ensure lightning-fast app response times for rural users with high latency.

9. Security & Compliance

When developing software for microfinance, your security must be proactive:

Encryption

AES-256 for data at rest and TLS 1.3 for data in transit. Zero-trust architecture is the baseline.

Identity Management

OAuth 2.0 and OpenID Connect, paired with Biometric MFA (FaceID/Fingerprint).

Compliance Tools

KYC/AML: Tools like Sumsub or ComplyAdvantage for real-time global sanctions screening.

Data Sovereignty: Automated geo-fencing to ensure data stays within local borders (e.g., GDPR in Europe or RBI guidelines in India).

Audit Trails

Immutable logs (often using private blockchain ledgers) to track every cent from disbursement to final repayment.

Cost of Microfinance Banking Software Development

The cost of microfinance banking software development varies based on your project’s scope and technical requirements.

Key Cost Factors

Feature Complexity

Basic lending modules are affordable, while AI-driven risk assessment and automated collections increase the budget.

Platform

Developing for both iOS and Android (via Flutter/React Native) or adding a web-based admin portal.

Team Location

Hourly rates fluctuate significantly between North America, European and Asian development hubs.

Integrations

Costs scale with the number of third-party APIs for KYC, payment gateways and credit bureaus.

For those looking to build a Neolending niche product, the cost to develop an app like EarnIn typically ranges from $20,000 to $60,000, depending on the specific feature set and integration complexity.

Challenges in Microfinance Software Development

Developing microfinance application software involves navigating high-stakes technical and legal hurdles that don't exist in standard app development. Addressing these four challenges early is the key to a successful launch.

1. Regulatory Compliance

Navigating complex, region-specific financial laws, including lending caps and strict KYC/AML mandates, to avoid heavy fines or legal shutdowns.

2. Data Security

Protecting sensitive personal and financial data from cyber threats using zero trust architecture, biometric MFA, and end-to-end encryption.

3. Legal System Integration

Building custom API middleware to connect modern mobile interfaces with rigid, outdated on-premises databases used by older institutions.

4. Low Connectivity Hurdles

Engineering offline first functionality and local data sync to ensure the app remains functional in rural areas with poor signals.

Strategic Use Cases for Microfinance Software

1. Earned Wage Access (EWA)

Enables employees to withdraw accrued wages before payday to cover immediate expenses, a model popularized by EarnIn.

2. Peer-to-Peer (P2P) Lending

Digital marketplaces that connect individual lenders directly with borrowers, automating contract generation and repayment distribution.

3. Agricultural Micro-Lending

Specialized credit for farmers with repayment schedules aligned to harvest cycles, often integrated with satellite weather data.

4. Group/Community Lending

Digitalizes traditional Joint Liability models, where social circles provide collective collateral and peer-based repayment pressure.

5. MSME Working Capital

Providing small business owners with instant liquidity based on real-time Point-of-Sale (POS) transaction history.

6. Emergency Overdraft Protection

AI-driven apps like Brigit that predict low balances and offer interest-free advances to prevent bank fees.

Future Trends in Microfinance Technology

1. AI & Machine Learning in Credit Scoring

Advanced algorithms now process non-traditional data like mobile usage and psychometric testing to provide instant, accurate risk profiles for unbanked individuals.

2. Blockchain for Secure Transactions

Decentralized ledgers are increasingly used in microfinance management software development to create immutable audit trails, reduce fraud, and lower cross-border settlement costs.

3. Digital Wallets & Embedded Finance

Credit is becoming invisible, with micro-loans integrated directly into grocery or delivery apps, allowing users to access funds at the exact point of need.

4. Open Banking APIs

Standardized data sharing enables microfinance banking software development to pull real-time financial history from multiple sources, ensuring faster approvals and more personalized interest rates.

5. Biometric Identity Verification

High-security facial and voice recognition are replacing traditional passwords, making financial tools more accessible to rural populations with low literacy rates.

Conclusion

Digital transformation is no longer optional for modern lending. By investing in specialized microfinance banking software development, institutions can bridge the financial inclusion gap through AI-driven insights and mobile-first accessibility. Whether you are a startup or an established MFI, partnering with an experienced fintech software development company ensures your platform remains secure, compliant and scalable in an increasingly competitive global market.

Launch Your Fintech Product

Turn your microfinance idea into a secure, scalable digital platform

FAQs

1. Is it better to buy or build microfinance software?

Building offers custom competitive advantages, AI ownership and tailored scalability but requires significant time and capital. Buying is faster and cheaper for startups. Generally, build if you need unique, proprietary features; buy if you require rapid market entry.

2. What are the security requirements for microfinance software?

Microfinance security requires AES-256 encryption, zero trust architecture and biometric MFA to protect sensitive data. Compliance with KYC/AML regulations and GDPR/local data laws is mandatory, along with immutable audit trails to track microtransactions and prevent internal fraud.

3. Can microfinance software integrate biometric authentication?

Modern microfinance banking software development seamlessly integrates biometric authentication (fingerprint, facial and voice recognition) via mobile APIs. This eliminates password barriers for rural or low-literate users, enhances security against fraud, and ensures rapid, one-touch transaction verification.

4. How to integrate mobile money APIs into microfinance software?

To integrate mobile money APIs into your microfinance software:

- Register: Obtain API credentials from providers (e.g., M-Pesa, MTN MoMo).

- Connect: Use RESTful APIs to initiate STK Push (collections) or B2C transfers (disbursements).

- Secure: Configure webhooks for real-time transaction confirmation and implement idempotency keys to prevent double payments.

5. How does AI improve credit scoring for borrowers without a history?

AI analyses alternative data, such as utility bills, mobile usage, and social behaviour, to build trust profiles. Machine learning patterns then predict creditworthiness for those lacking traditional history, enabling faster, more accurate risk assessment and broader financial inclusion for unbanked borrowers.