Traditional banking infrastructure is crumbling under its own weight. Branches cost banks an average of $3 million per year to maintain, and yet 73% of customers aged 40 and under have not set foot in a branch over the last year (McKinsey, 2025). In other words, customers are leaving the brick-and-mortar bank buildings, not the banks themselves.

Virtual banking apps used to be convenient additions to an already existing banking service. But now they serve as the core banking channel for 2.3 billion people worldwide. As early as 2026, neobanks have already managed to secure 24% of the market share in retail banking among developed countries, and that number is expected to increase to 40% by 2028 (Deloitte Digital Banking Report, 2026).

Let's break down the numbers:

- In the Digital Banks market, the projected Net Interest Income worldwide is set to reach US$1.66 trillion (Statista, 2026)

- 47% lower customer acquisition costs compared to traditional banks (Accenture)

- 89% customer satisfaction vs. 62% for traditional banks (J.D. Power Banking Study)

- 3-5x faster account opening and loan approvals via mobile app

If you're a financial institution, fintech startup, or enterprise exploring digital transformation, virtual banking app development is no longer optional, it's existential. This comprehensive guide breaks down everything you need to build a secure, scalable, regulation-compliant virtual banking platform that customers trust and regulators approve.

What Is a Virtual Banking App? (And Why "Mobile Banking" Isn't Enough)

A virtual banking application can be defined as an electronic application where customers can carry out all functions of banking, including account maintenance, transfers, borrowing, and savings, among others, without necessarily visiting the bank offices.

Virtual Banking vs. Mobile Banking vs. Neobanking: The Critical Differences

| Feature | Mobile Banking App | Virtual Banking App | Neobank |

| Purpose | Companion to physical bank | Standalone digital bank | Digital-only bank (no branches) |

| Account Opening | Must visit branch first | Fully digital onboarding | 100% digital, no physical presence |

| Services | Limited (checking, transfers) | Full banking suite | Full suite + advanced features |

| Infrastructure | Bolt-on to legacy systems | Modern core banking system | Cloud-native, API-first architecture |

| Regulatory Status | Licensed traditional bank | Licensed bank (digital channel) | Licensed bank or partner with one |

| Examples | Chase Mobile, Wells Fargo app | Marcus by Goldman Sachs, Ally Bank | Chime, Revolut, N26, Monzo |

Embark Your Virtual Banking App Development Journey With Us

At Suffescom, we follow an agile methodology for the development process, and our virtual banking app development cost is pocket friendly. Get in touch with our experts today.

Why Traditional Banks and Startups Are Racing to Build Virtual Banking Apps

The financial services industry is undergoing the most significant transformation since ATMs were introduced in the 1960s. Here's why virtual banking app development has become the top strategic priority:

1. Customer Behavior Has Irreversibly Shifted

The Data:

- 78% of U.S. consumers use mobile banking apps weekly (Federal Reserve, 2025)

- 45% would switch banks for better digital experience (Salesforce Financial Services Report)

- Gen Z (born 1997-2012) expects instant everything: instant account opening, instant loans, instant support

The Implication: Banks without world-class virtual apps are bleeding young customers to neobanks at alarming rates.

2. Operational Cost Savings Are Massive

Traditional Bank Branch Economics:

- Average cost per transaction: $4.25

- Annual branch operating cost: $3 million

- Customer acquisition cost: $350

Virtual Banking App Economics:

- Average cost per transaction: $0.08 (98% reduction)

- Annual app operating cost: $400,000 (87% reduction)

- Customer acquisition cost: $50-$100 (71-85% reduction)

Real-World Example: Marcus by Goldman Sachs achieved profitability in 3 years vs. the industry average of 7-10 years for traditional branch expansion.

3. Revenue Opportunities Beyond Traditional Banking

Virtual banking apps unlock revenue streams impossible in branch-based models:

- Embedded Finance – Integrate banking into non-bank apps (Uber's payment card, Shopify Capital)

- BaaS (Banking-as-a-Service) – White-label banking infrastructure for fintechs

- Subscription Models – Premium tiers with advanced features ($9.99/month like Revolut Metal)

- Data Monetization – Anonymized insights for merchants and partners (GDPR-compliant)

- Micro-Transaction Fees – Fraction-of-a-cent fees that scale to millions at digital volume

- API Monetization – Developer access to banking APIs

Market Size: BaaS alone is projected to reach $74.6 billion by 2030 (Fortune Business Insights).

4. Regulatory Frameworks Now Support (and Encourage) Digital Banking

Major Regulatory Milestones (2024-2026):

- European Union: Revised Payment Services Directive (PSD3) mandates open banking APIs

- United States: OCC grants national bank charters to fintech companies

- United Kingdom: FCA accelerates digital bank licensing (62 approvals since 2020)

- Singapore: MAS Digital Bank Framework enables app-only banking licenses

- India: RBI issues 12 new digital banking licenses in 2025

Implication: Regulatory barriers that once protected incumbents now create opportunities for nimble digital challengers.

Core Features That Need To Be Integrated Into Modern Virtual Bank App In 2026

While a modern online banking application should be capable of executing financial operations smoothly, these key features will ensure a seamless experience, regulatory compliance, and higher user retention rate.

1. Instant Digital Account Opening

Allowing customers to open bank accounts instantly and automatically by using e-KYC, AI-powered document verification, biometric recognition, and risk assessment is a requirement for any advanced virtual banking platform.

2. Multi-Currency Accounts and Cross-Border Remittances

Multi-currency accounts, virtual IBANs, as well as real-time cross-border transfers with transparent foreign exchange services should become an integral part of the platform's functionality. The inclusion of this feature will improve accessibility and reduce the cost of money transfers.

3. Fast Peer-to-Peer Transactions and Wallets

Instant P2P transfers, QR code payments, payments requests, as well as digital wallets are the essential characteristics that will make banking convenient for customers.

4. Advanced Personal Finances Management with the Help of AI

Personal finances management is made easy by incorporating AI-based technologies, which help to classify transactions, suggest ways to optimize spending, automate saving processes, and control subscriptions.

5. Embedded Lending (Instant Loans & Credit)

Embed digital lending modules such as instant loans, pre-approved credit lines, BNPL services, and micro-loans into the banking ecosystem. This expands financial service offerings while creating additional revenue opportunities.

6. Investment & Wealth Management

Integrate robo-advisory tools, digital asset management, stock trading, and goal-based investment features into the platform. These capabilities transform a banking app into a comprehensive wealth management solution.

7. 24/7 AI Customer Support

Deploy AI-powered chatbots, natural language banking assistance, and multilingual support to provide round-the-clock customer service. This improves operational efficiency while enhancing response times and customer satisfaction.

8. Biometric Authentication & Security

Strengthen platform security through fingerprint authentication, Face ID, behavioral biometrics, and device binding controls. These advanced security layers significantly reduce fraud risks while improving secure user access.

9. Open Banking & Third-Party Integrations

Enable open banking connectivity through account aggregation, API access, financial marketplaces, and secure third-party integrations. This creates a scalable banking ecosystem while supporting interoperability and embedded finance models.

10. Gamification & Social Features

Introduce savings challenges, social goal tracking, reward-driven financial literacy modules, and engagement-led gamification mechanics. These features increase user retention while making digital banking more interactive.

11. Environmental & Social Impact Tracking

Incorporate sustainability-focused features such as carbon tracking, ESG investment options, sustainable spending insights, and charitable giving tools. This helps align banking services with growing demand for socially responsible finance.

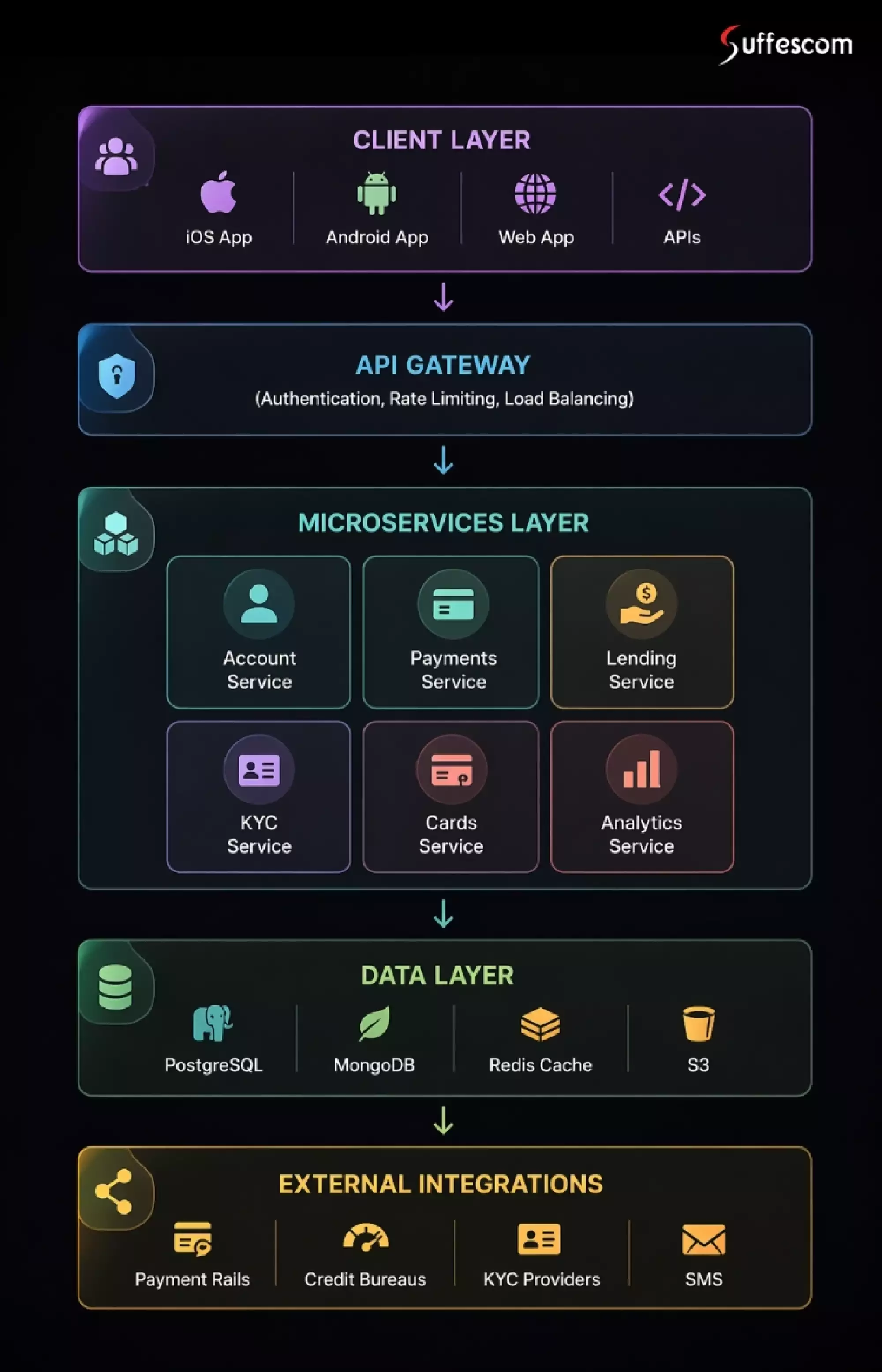

Virtual Banking App Development: The Technology Architecture

Building a secure, scalable virtual banking platform requires sophisticated technical infrastructure that balances innovation with regulatory compliance.

One-Stop Solution For Your Virtual Banking App Solutions

We are a leading development company that provides all-in-one virtual banking app development solutions with customized features and functionalities.

Benefits of Virtual Banking App Development

Virtual banking app development offers businesses numerous benefits that can significantly boost their revenue. Let’s have a look at some of them:

Cost Reduction

No buildings or branches exist, so renting or maintaining a place is unnecessary. Most processes, like opening an account or conducting international payments, can be done online. Traditionally this includes a lot of expenses, which now can be converted to your savings.

Blockchain Aided Security

With its decentralized and immutable ledger, blockchain technology adds a layer of security and transparency to virtual banking. By leveraging blockchain, virtual banking apps can offer enhanced security for user transactions and data, eliminating the need for intermediaries. Additionally, blockchain enables cryptocurrencies within the virtual banking ecosystem, allowing users to transact using digital assets.

Digital Currency

The best part about virtual banking is that it can support cryptocurrency payments. With crypto banking platforms solutions, users can exchange cryptocurrencies such as bitcoin, binance coin, and more. In contrast to deposits, it makes it possible for central banks, private citizens, and non-banking financial institutions to settle money immediately. As a result, the payment system's concentration of liquidity and credit risk is constrained. Using digital currencies allows for the quickest and least expensive money transfers.

Immersive Banking Experience

By going virtual, you will be providing your customers with an immersive banking experience where they will interact with you in a virtual space. It will be exciting for customers; they will be excited to be a part of such an experience. In this way, you can enhance customer engagement and satisfaction. Moreover, more and more customers will be attracted to be a part of your virtual bank.

Virtual Banking App Development Process: 7 Phases to Launch

The virtual banking app development process can vary as per individual needs and requirements. At Suffescom, we follow the following development procedure:

Devise Strategy

The first step in building your virtual banking app is to create a strategy. First, we thoroughly research your competitors, understand customer needs, and more. Also, we listen to all of your business requirements and devise a development plan.

UI/UX Design

Your virtual banking app must look attractive to give your users the best banking experience. Our designers design your application in a way that catches the users' attention. We integrate the latest features and functionalities into the app that makes it stand out from others.

Integration Of Technologies

To give your users an immersive experience, we integrate the latest technologies, such as metaverse, blockchain, smart contracts, AR/VR, and cryptocurrency. These technologies are the backbone of creating a real-world experience in a virtual world.

Development

After we are done integrating the latest technologies, we start the development of your bank in the metaverse. We follow your business requirements and create a front/back end that aligns with your business image perfectly.

Quality Assurance

Next, our QA team conducts different types of testing on your virtual bank platform, such as performance, usability, speed, and functional testing. We ensure that the platform is working as intended without any vulnerabilities and bugs.

Deployment

Once you approve the virtual bank platform, we deploy it across various platforms and devices. We ensure it is compatible across various devices and provide a smooth and seamless user experience.

Post-Launch Support

Our work doesn’t end after the launch of your platform. We continuously monitor your virtual bank platform and ensure it remains flawless and bug-free. Also, we keep upgrading your platform with advancements in market trends and technologies.

Advanced Architecture Features for Scalable Virtual Banking Platforms

This layer defines the core engineering strength of a virtual banking system, focusing on scalability, modularity, and real-time financial processing. It differentiates enterprise-grade solutions from basic fintech applications.

Banking Architecture Based on Microservices

Consists of individual services that can be independently updated and upgraded. It helps in making updates quickly without bringing down the whole system.

Transaction Processing with an Event-Driven Architecture

Facilitates the real-time processing of various financial transactions. It ensures fast and consistent system performance.

Cloud-Native Scalable Infrastructure

Developed using cloud platforms, which makes it easy to scale according to the amount of traffic generated. It increases system efficiency and reliability.

Real-Time Financial Ledger Sync Engine

Ensures constant synchronization of information about all finances and transactions. It facilitates accurate financial reporting.

Banking Architecture with Emphasis on APIs

Is focused on building a banking system on API-based architecture, facilitating smooth integration with other fintech solutions.

Support for Multi-Tenant Banking Systems

Provides the capability of hosting different banks or business accounts in one system while keeping their data separate from others.

Technology Stack for Virtual Banking App Development

| Layer | Technology | Purpose |

| Frontend | React.js / Next.js | Builds responsive, high-performance banking dashboards and web interfaces |

| Frontend (Mobile) | Flutter / React Native | Enables cross-platform mobile banking applications for iOS and Android |

| Backend | Node.js / Java (Spring Boot) / Go | Powers secure APIs, transaction processing, and core banking logic |

| AI & Analytics | Python | Used for fraud detection, credit scoring, and predictive financial analytics |

| Databases | PostgreSQL / MongoDB / Cassandra | Manages structured and unstructured financial data at scale |

| Cache Layer | Redis | Enables real-time transaction speed and session management |

| Cloud Infrastructure | AWS / Microsoft Azure / Google Cloud | Provides scalable, secure, and highly available banking infrastructure |

| Containerization | Docker | Ensures consistent deployment of microservices across environments |

| Orchestration | Kubernetes | Manages scaling and deployment of distributed banking services |

| API Layer | REST / GraphQL | Enables seamless integration with third-party fintech services |

| Authentication | OAuth 2.0 / JWT | Ensures secure user authentication and session control |

Cost of Virtual Banking App Development

The cost of building a virtual banking application depends on multiple technical, regulatory, and architectural factors. These include feature complexity, security implementation, third-party integrations, and scalability requirements.

Estimated Development Cost Range

| App Type | Estimated Cost | Description |

| MVP-Level Virtual Banking App | $25,000 – $35,000 | Basic banking features such as user onboarding, wallet management, fund transfers, and simple dashboards. |

| Mid-Level Digital Banking Platform | $35,000 – $50,000 | Includes KYC/AML integration, multi-currency support, API integrations, and fraud detection systems. |

| Enterprise-Grade Banking System | $50,000 – $60,000+ | Advanced architecture with AI-driven analytics, blockchain integration, multi-region compliance, and high scalability. |

Key Factors Affecting Development Cost

Features Complexity

The more complex the feature set with systems like lending, forex trading, investments etc., the higher the development cost and efforts. Complex systems demand sophisticated backend implementation and testing.

Compliance & Security

The implementation of standards such as KYC, AML, PCI DSS, and GDPR, among others affects the overall development cost. Security architecture and compliance preparation complicate the development process.

Tech Stack & Architecture

Microservices architecture, cloud-based systems, and real-time implementations demand high costs for engineering compared to monolithic architectures.

Integration With Third-Party Services

Integrating services from third parties such as payment gateways, banking systems, IDV providers, and forex systems demands higher development efforts and licensing fees.

Performance & Scalability

Systems that can handle millions of transactions per second need distributed infrastructure, efficient load balancing, and high performance database management systems.

Industry Use Cases of Virtual Banking App Development

Explore how virtual banking applications power diverse use cases across retail banking, fintech, payments, enterprise treasury, and embedded finance ecosystems.

Digitized Retail Banking

It helps digitize traditional banking processes and services with the help of account management and real-time onboarding of customers. In addition, it provides an improved user experience since it does not require visits to the physical branch.

Neobank App Development Solutions

Businesses looking to launch fully digital banks often partner with a Neobank App Development Company to build scalable, regulation-ready banking ecosystems without relying on traditional infrastructure. These platforms can support digital accounts, cross-border payments, lending services, and other advanced financial products for modern neobank operations.

Cross-Border Payment Ecosystem

It is helpful in making international payments quickly and securely. It provides multiple currencies and faster settlements in such transactions than traditional banking services, which delay and charge extra fees for them.

Corporate Treasury Management

It allows the enterprise customers to manage their liquidity and financial performance using integrated dashboards.

Digital Wallet Banking Solutions

Involves the integration of digital wallet payment solutions that allow instant transfers and payments to be made.

Embedded Finance Integration

It allows the embedding of financial services within third-party applications to provide seamless experiences. For example, payment and lending can take place within third-party applications themselves.

Compliance, Security, and Regulatory Framework for Virtual Banking

Build regulation-ready virtual banking platforms with robust compliance frameworks, advanced security controls, and globally aligned financial standards.

Digital Banking Architecture Compatible with RBI

Makes the platform follow central bank regulations for conducting safe and legitimate financial operations. It supports compliance with national banking regulations.

Identity Verification & Anti-Money Laundering

Automatically verifies identities and implements anti-money laundering policies at the time of transaction. It aids in fraud detection and regulatory compliance.

GDPR/Personal Data Protection Compliance

Make sure that users' information remains protected in accordance with worldwide personal data protection laws like GDPR. It maintains the security of data.

PCI DSS Payment Card Data Protection

Provides security for payment card transactions via globally accepted guidelines. It lowers the chances of card-based fraud.

SOC2/ISO 27001 Compliance

Guarantees robust data protection measures and high levels of reliability in system operations. It confirms the operational effectiveness via globally recognized certifications.

Transaction Monitoring & Fraud Prevention

Constantly monitors the financial activities to detect any unusual patterns in real-time. It improves platform security and mitigates financial risks.

Scalable Revenue Strategies for Virtual Banking Apps

Discover scalable monetization models that help virtual banking platforms generate revenue through payments, lending, subscriptions, and API-driven ecosystems.

Interchange Fees

Generates income by charging fees on each transaction or transfer done via cards. This is one of the widely used revenue streams in digital banking.

Subscription-Based Neobanks

Involves providing superior financial services by subscription per month or year. This helps the platforms ensure regular flow of income.

Currency Exchange Margins

Gains income from the margin of exchange of foreign currencies during cross-border transactions. It is very relevant for international banks.

Interest Margin Revenue

Gains income from differences in interest rates for loans and repayments. This is a crucial part of the monetization process.

Superior Banking Features

Involves offering advanced banking features such as analytics. This strategy promotes subscription services and upgrades.

Third-Party App Integration Fees

Fees charged to third parties using banking APIs. It is a good way to generate income in an ecosystem-based system.

Hire The Best Virtual Banking App Development Company

Suffescom is your ultimate partner when it comes to developing your virtual banking application. We know the ins and outs of the development process and can help you build a highly scalable virtual banking application

Hire Suffescom- The Best Virtual Banking App Development Company

As an experienced virtual banking app development company, Suffescom helps businesses launch next-generation banking solutions powered by advanced technology, regulatory readiness, and scalable architecture.

Industry Expertise

We have more than 13+ years of experience in blockchain, metaverse, AR/VR, and more, which gives us an edge over other development companies in the industry. We have built many virtual apps for our clients globally, and we can build yours too.

Customized Solutions

We will listen to your project requirements and build a customized virtual banking application. We add the features you wish to your application and use your preferred technologies and blockchain networks.

On-Time Delivery

We ensure that we deliver your project on time without delays or cancellations. We make sure to meet your expectations and deliver your project as discussed.

Leading Technology

Our team of virtual banking app developers stays up-to-date with emerging technology and utilizes it in your app development. You can make sure that your banking app meets the market standards.

Developing a Scalable Architecture

We develop cloud-native banking solutions using the latest microservices technology, making them ideal to support high-volume transactions and scalable in nature.

Support and Maintenance

Not only do we deploy our solutions, but we also provide support to ensure the optimization, security, and competitiveness of your virtual banking platform.

FAQs

1. How long would it take to create a virtual banking app?

It depends on the complexity of the project. The creation time of a minimum viable product (MVP) with basic functionality (account management, KYC, and payments) takes about 3–5 months. Developing a full-fledged neobank platform with artificial intelligence, open banking APIs, and multi-currency support takes 12–24 months. Suffescom applies a modular app development approach, which allows speeding up the release by 30–40% compared to conventional development.

2. How much will it cost to create a virtual banking app?

The budget varies between $25,000 and over $60,000+, depending on the required features and functionality, compliance requirements, targeted platforms (iOS, Android, Web), and AI capabilities. Consult our team to get a customized price estimate for your project.

3. Which licenses are required to launch a virtual bank?

This question is relevant for different countries, where licensing procedures differ. In India, one might need to obtain an NBFC or payment aggregator license from the RBI. In the United Kingdom, an e-money institution (EMI) license from the FCA should be secured.

4. Can you integrate a virtual banking app with existing core banking systems?

Yes. Suffescom has extensive experience integrating with major core banking systems, including Temenos T24, Finastra, Infosys Finacle, and Oracle FLEXCUBE, as well as custom legacy systems. We use API middleware and event-driven architecture to ensure seamless data synchronization without disrupting existing operations.

5. How do you ensure the security of a virtual banking app?

Our security framework includes end-to-end encryption (AES-256, TLS 1.3), biometric authentication, multi-factor authentication (MFA), real-time fraud detection using ML models, and Hardware Security Module (HSM) integration for cryptographic key management. Every app undergoes VAPT (Vulnerability Assessment and Penetration Testing) before launch.

6. Do you offer white-label virtual banking solutions?

Yes. We offer both white-label banking platforms (ready to deploy in 4–8 weeks with your branding) and fully custom-built solutions. White-label solutions are ideal for startups and fintechs looking to go to market quickly, while custom builds are recommended for enterprises requiring unique feature sets and deep system integrations.

7. What post-launch support do you provide?

Suffescom provides comprehensive post-launch support, including 24/7 technical monitoring, bug fixes (within SLA timelines), performance optimization, security patches, and feature enhancements. We offer flexible support plans: monthly retainers, quarterly update packages, and dedicated development team extensions.