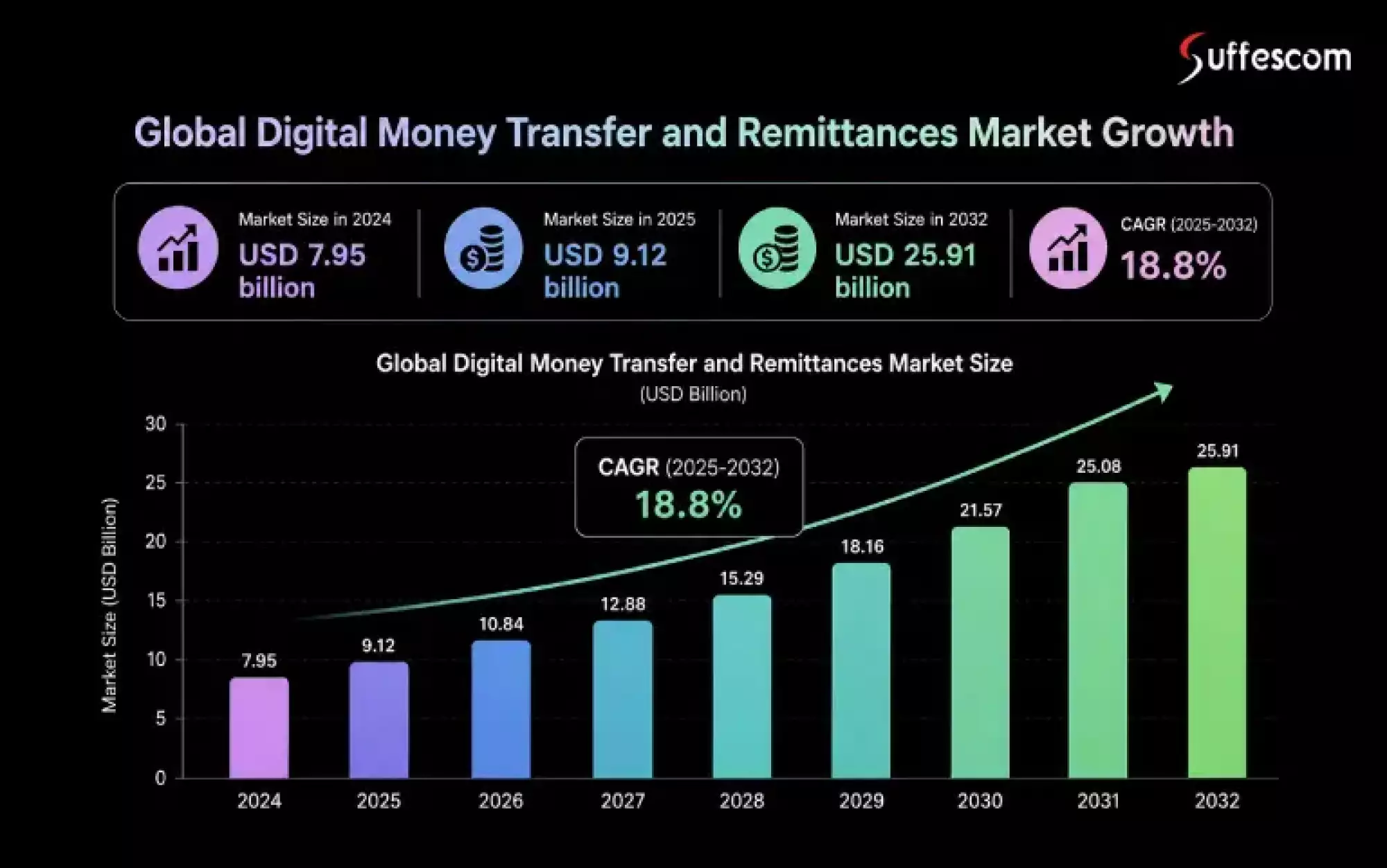

The world moves money differently today. Whether someone is splitting a dinner bill, supporting family overseas, or paying a remote contractor, digital transfers have become the default. According to StatsMarketResearch, the global digital money transfer and remittances market size was valued at USD 7.95 billion in 2024. The market is projected to grow from USD 9.12 billion in 2025 to USD 25.91 billion by 2032, exhibiting a robust CAGR of 18.8% during the forecast period.

Behind this growth lies a clear opportunity: businesses, fintech startups, and financial institutions worldwide are actively investing in money transfer application development to capture a share of this rapidly expanding market. From remittance app development catering to migrant workers to custom money transfer apps serving specific business niches, the demand spans every segment.

This guide walks you through everything you need to know about what a money transfer app is, how to build one from scratch, what it costs, and how to navigate the regulatory landscape. Whether you're a startup founder or a product leader at an established company, this is your go-to resource for money transfer app development.

What Are Money Transfer Apps?

Money transfer apps are software applications designed to allow people to perform electronic fund transfers through their smartphones, tablets, or computer browsers without having to make physical visits to bank branches or handle any cash at all.

At the end of the day, money transfer apps are nothing more than an intermediate layer between people and the actual money transfer process itself.

When a person signs up for a money transfer app, verifies their identity, links their bank account, debit card, or e-wallet, makes transfers, and tracks the status of transactions, the app takes care of everything behind the scenes, including foreign exchange transactions and fraud protection.

Types of Money Transfer Apps: Which Category Should You Build?

Discover the most widely used digital payment solutions across industries. Build the right app category to maximize adoption and scalability.

P2P (Peer-to-Peer) Payment Apps

Allow individuals to send money directly to one another using a phone number, email, or username. Examples: Venmo, Cash App, Zelle

Remittance / International Transfer Apps

It is built for cross-border transfers with currency conversion. Examples: Wise, Remitly, Western Union Digital.

B2B Payment Platforms

It is designed for business-to-business transactions, vendor payments, and payroll. Examples: Tipalti, Airwallex.

Digital Wallet Apps

Combines stored-value wallets with transfer functionality. Examples: PayPal, Google Pay, Apple Pay. If you're building in this category, PhonePe-style payment apps are a fast-to-market starting point.

Key Features of Money Transfer Application Development

Core functionalities required to build secure, scalable, and high-performance payment solutions.

Must Have Features

User Registration & KYC Verification: Multi-stage registration procedure including identity verification through scanning of governmental IDs, face matching against selfies, document validation, and geographic AML/OFAC screening. A geography-dependent verification process allows adaptation to the KYC requirements according to the jurisdiction of the user. Valid registrations can be approved programmatically without human intervention for lower-risk users.

Account & Profile Management: Features include account creation, storage and editing personal information, adding billing addresses, linking bank accounts, and storing card data. Multi-language support is crucial for the success of remittance-oriented applications. A complete audit trail of all actions related to the account needs to be maintained to ensure compliance with regulations and fraud investigations.

Bank Account & Card Integration: Features to integrate with bank accounts using ACH/SEPA connection (via Plaid, TrueLayer, or own API), debit/credit card top-ups, and loading of wallets from in-app transactions. SWIFT/IBAN support should be present to process international money transfers.

Funds Transfer & Payment Initiation: The key flow of the application includes recipient selection (either by name, phone number, or account number, SWIFT/IBAN), specifying the amount of funds to send, selecting the transfer method, confirming transfer fees and currency exchange rate, and confirming.

Multi-Currency Payments & Forex Conversion: Integration of live exchange rates, upfront cost information before transaction confirmation, and real-time forex conversion. Important for cross-border remittances.

Real-Time Transaction Status: Push notification services, in-app transaction tracking (Initiation → Processing → In Transit → Delivery) with time-stamped logs. Creates trust among users and minimizes customer care support requirements.

Payment Statements & History: Searchable payment history, payment categorization tools, generation of payment statements in PDF and CSV format, and recurring payments information. Helps in financial management and compliance with legal requirements.

Two-Factor Authentication (2FA): SMS one-time password, TOTP from authenticator application, and face/fingerprint identification. Use of biometric identification is now considered mandatory for consumer-facing money transfer applications.

Notifications & Alerts In-App: Transaction-related notifications, security notifications, and promotional notifications sent via push, email, and SMS notifications.

Advanced Features

AI-based Fraud Detection: Real-time transaction scoring that utilizes machine learning models to detect any anomalies before completing a transaction. This behavioral analysis, device fingerprinting, and velocity checks enable the reduction of fraud while not impeding legitimate users.

Split Payments and Group Expense Management: Enable splitting bills, sending requests for money to different contacts, and keeping track of group balances. This is a highly valued addition in P2P applications targeted at young consumers.

Scheduled and Recurring Transfers: Allow automating repetitive payments, standing orders, and monthly remittances. This is especially important for users transferring money to their relatives regularly.

In-App Customer Support (Chatbot + Human): Automated assistance in answering typical inquiries (transfer status, fee information, account limitations) with an escalation option to human agents. The cost of customer service will be reduced considerably.

Loyalty Programs: Offer gamification elements, cashback on transferred funds, and referral bonuses. An efficient growth strategy that has been successfully implemented by both Remitly and Wise.

Cryptocurrency and Stablecoins Deposit/Transfer: Accept deposits of Bitcoin/USDT and enable exchange between coins and local currency. Valuable for fintech solutions targeting tech-savvy consumers or users from regions with poor local banking services.

In-App Cards: Issue prepaid debit cards linked to in-app wallets. Differentiates your money transfer software as a broader financial platform.

Open Banking Integrations: Connect to users' bank accounts via open banking APIs (PSD2 in Europe, CDR in Australia) for real-time balance checks and account-to-account transfers without manual card entry.

Admin Panel Features

KYC/AML Dashboard: Inspect suspicious accounts, authorize or deny KYC checks, allocate risk categories, and keep a comprehensive audit log for regulator scrutiny.

Transaction Monitoring and SAR Filing Tools: Monitor all transactions in real time with automated alerting based on thresholds. SAR filing capabilities automate compliance activities.

Fee Structure and Exchange Rates Settings: Adjust maximum limits for transfers, configure fees by route or customer category, and modify FX margins without programmer assistance.

Customer Management and Account Control: Suspend accounts, upgrade tiers, perform manual KYC bypasses, and handle customer support tickets.

Performance Metrics Dashboard: Analyze volumes, generate revenue reports, assess corridor efficiency, and conduct customer group analysis.

Validate Your Money Transfer App Idea

Not sure where to start? We’ll help you define the right features, tech stack, and compliance roadmap.

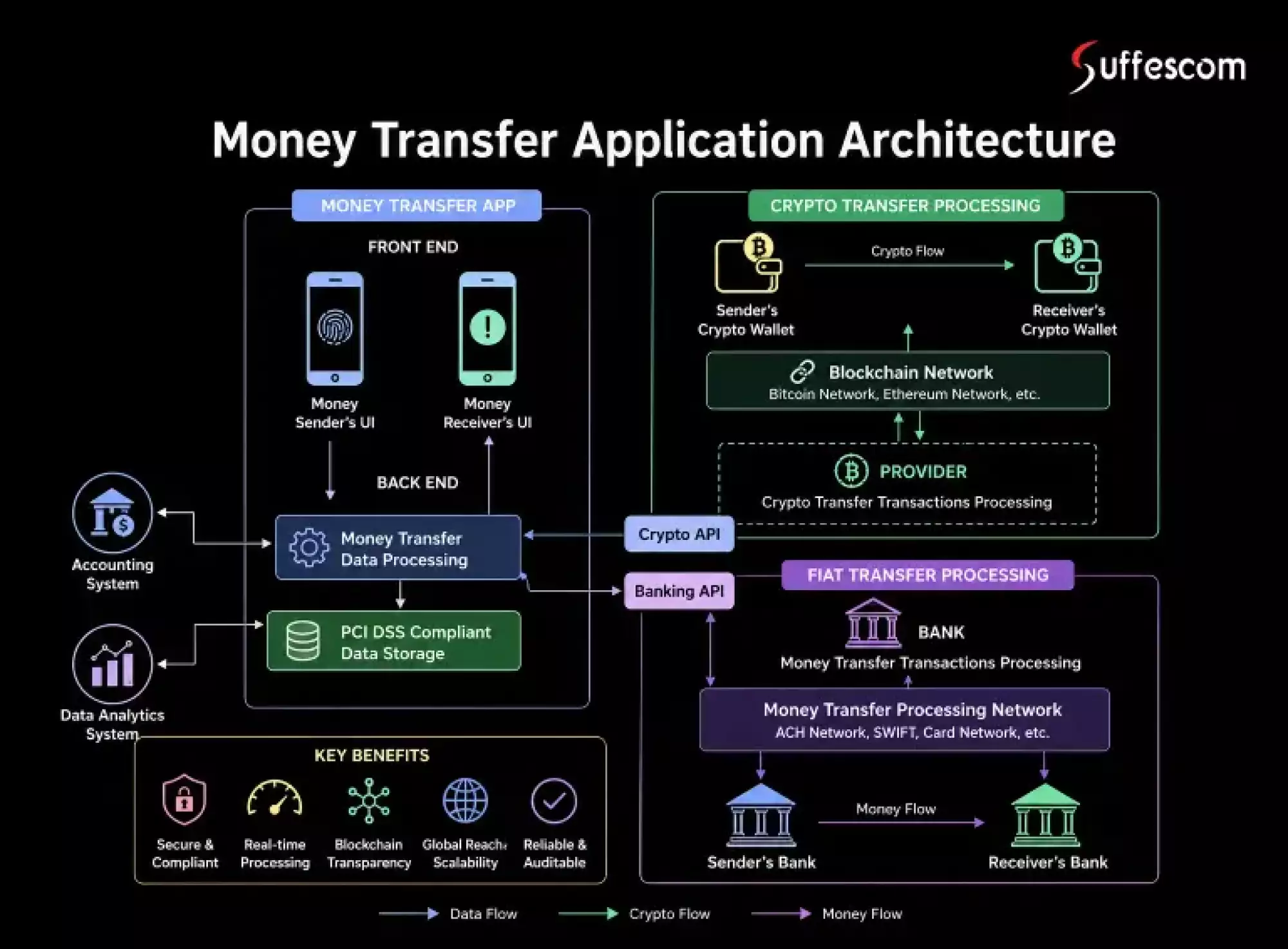

Core Architecture of Money Transfer Application Development

Enables secure, real-time transaction processing across banking and digital networks. It is designed to ensure scalability, compliance, and seamless global fund transfers.

- User Interface: Enables users to send, receive, and track payments.

- Backend Engine: Processes transactions and manages business logic.

- Data Storage: Secure, compliant storage for user and transaction data.

- Banking Integration: Connects with banks and payment networks for fund transfers.

- Crypto Layer (Optional): Supports blockchain-based transactions via wallets and APIs.

- Processing Network: Routes payments between sender and receiver accounts.

- Integrations: Connects with analytics, accounting, and compliance tools.

- Security Layer: Ensures encryption, authentication, and fraud prevention.

Steps To Take When Creating A Money Transfer App: The Full Guide

Creating a money transfer app will be more complicated than creating an ordinary mobile app. You have to know regulations, be a cybersecurity expert, and properly integrate with financial services. Here is the full guide.

Step 1: Do Market Research & Determine Your Target Audience

The first thing you have to do before writing even a line of code is to research your market thoroughly. Who is your target audience? Will it be people without bank accounts in developing countries? Workers who send money home from abroad? Do companies need to pay their vendors in other countries?

Do competitor analysis on PayPal, Wise, and Remitly. Figure out what they are good at, what features they offer, and where they lack. Analyze possible customers' needs to understand how they would want you to develop the app.

Step 2: Determine the Type of Money Transfer App You Will Be Making

This step helps you determine your development process, necessary regulations, and ways to monetize your app. There are various kinds of money transfer apps that are made for different purposes. Consider whether your money transfer app is going to be used domestically or internationally.

Step 3: Regulatory Compliance and Licensing

It's the step that gets the most oversight and deserves it, while creating a money transfer app. Running a money transfer service without the right licenses will be illegal in most jurisdictions.

- Registering with FinCEN as an MSB + Money Transmitter Licenses (MTLs) in all the states where you do business - United States

- Compliance with PSD2 + EMI license + AML/KYC requirements according to AMLD5 - European Union

- RBI Authorization as per Payment and Settlement Systems Act 2007 - India

- FATF recommendations + SWIFT + country-specific regulations - Globally

Pro tip: Factor regulatory compliance into your budget from day one. The costs associated with obtaining licenses + hiring legal and compliance specialists + building AML/KYC infrastructure usually come up to 20–30% of your overall project budget for a remittance app.

Step 4: UI/UX Design

People ditch money transfer services at any point of difficulty. For this reason, your UX design needs to be clear, quick, and trusted. Main UX design requirements for a money transfer mobile app include:

- Minimizing the number of clicks necessary to send money (aim for 3-4 clicks).

- Transparency in exchange rates and fees charged before

Step 5: Technology Stack for Online Payment Transfer App Development

Choosing the right technology stack is foundational to your app's performance, scalability, and security. Here's what leading money transfer app development teams typically use:

| Layer | Recommended Technologies | Purpose |

| Mobile Frontend | React Native / Flutter | Cross-platform iOS & Android app development |

| Web Frontend | React.js / Vue.js | Web application and admin dashboard |

| Backend | Node.js / Python (Django) | API layer, business logic, transaction processing |

| Database | PostgreSQL / MongoDB | Storage of transactional and user data |

| Payment APIs | Stripe, Plaid, Dwolla | Bank connectivity, payment processing, and fund transfers |

| KYC/AML | Jumio, Onfido, Persona | Identity verification and compliance checks |

| Cloud | AWS / Google Cloud | Hosting, scalability, and infrastructure management |

| Security | TLS 1.3, AES-256, OAuth2 | Data encryption, authentication, and protection |

Step 6: Development & Third-Party Integrations

The development process normally uses Agile development with two-week sprints. The essential integrations that must be developed are payment gateway APIs (e.g., Stripe, Adyen); banking connectivity (Plaid, TrueLayer); know-your-customer providers (Onfido, Jumio); and push notifications (Firebase).

In relation to the development of a remittance app, additional components required are SWIFT/SEPA connectivity; foreign exchange rates API (Open Exchange Rates, XE); and sanctions databases (Dow Jones, Refinitiv).

Step 7: Security Implementation

Security in money transfer apps is non-negotiable in money transfer application development. One security breach could ruin your user trust and result in significant fines. Some critical security features are:

- Encrypt all data both in motion and at rest. End-to-End Encryption (TLS 1.3+AES-256)

- Help prevent fraud and improve the overall experience. Biometric Authentication (Fingerprint & Face ID)

- Eliminates exposure of personal financial data. Tokenization

- Machine learning algorithms will detect abnormal behavior. Real-time Fraud Detection

- Quarterly security reviews from trusted third parties (OWASP standards). Penetration Testing

- Required for all apps accepting credit or debit cards. PCI-DSS Compliance

Step 8: Testing, Launch & Post-Launch Support

Before going live, your app must pass rigorous testing: functional testing (all features work as intended), security testing (penetration tests, vulnerability scans), performance testing (load testing for peak transaction volumes), and regulatory testing (compliance review with legal counsel).

A soft launch to a limited user base is recommended before full market rollout. Post-launch, plan for ongoing maintenance, bug fixes, regulatory updates, and feature evolution based on user feedback.

Build Future-Ready Financial Solutions With Confidence

Suffescom delivers high-performance Money Transfer Applications engineered for accuracy, scalability, which adapt to evolving regulations, and complex financial ecosystems.

Money Transfer App Development Cost: Complete Breakdown

The cost to develop a money transfer application varies significantly based on scope, features, geography, and development team. Below is the most detailed cost breakdown available — including the hidden costs that most guides omit.

Cost Breakdown by App Tier

Basic MVP (Domestic P2P)

- $25K – $35K

- Core features: registration/KYC, bank linking, P2P transfer, notifications, basic transaction history. Single platform (iOS or Android). 3–5 month timeline.

Mid-Tier App (Multi-Feature)

- $35K – $45K

- MVP + multi-currency support, AI fraud detection, admin compliance panel, recurring transfers, chatbot support, cross-platform (iOS + Android + web). 5-8 month timeline.

Advanced Remittance Platform

- $45K – $60K

- Multi-rail routing, multi-payout methods, open banking integration, multi-jurisdiction compliance, AI analytics. 8-10 month timeline.

Enterprise-Grade Solution

- $60K – $80k+

- Full custom: 150+ currencies, real-time FX engine, global licensing support, white-label capability, dedicated fraud ops team. 10-12 month timeline.

What Our Clients Say

Suffescom maintains a 4.8+ star rating across Clutch, G2, DesignRush, and Trustpilot, which is driven by consistent delivery quality, transparent communication, and long-term client relationships. Here is what clients building payment and fintech solutions say about working with us:

Common Mistakes in Money Transfer Application Development

1. Treating Compliance as an Afterthought

The most expensive mistake. Completing the build and then discovering 18 months of licensing work is needed before launch is not hypothetical; it happens regularly. Engage a fintech compliance specialist in the discovery phase.

2. Underestimating KYC Friction Impact on Conversion

KYC drops off if poorly designed. Industry benchmark: 60–80% KYC completion rate. Below that, you're losing users before the first transfer. Use risk-tiered onboarding: basic verification for small initial transfers and full KYC to unlock higher limits. Our blockchain fintech solutions include a decentralized KYC process that reduces drop-off significantly.

3. Monolithic Architecture

A monolithic money transfer app is expensive and slow to scale. Use microservices from the start to separate services for user management, KYC, payment processing, fraud detection, and notifications. They work independently, are scalable, and are maintainable.

4. Single Payment Rail Dependency

Building on one payment rail creates a single point of failure. Design for multi-rail redundancy from the start; even if you use only one rail initially, the architecture must support adding a second without a major rebuild.

5. Underestimating Fraud Exposure at Launch

New apps face elevated fraud in months 1–12 before ML models are tuned on real data. Budget a 0.5–1% fraud reserve, implement conservative transaction limits at launch, and expand limits as your fraud models mature. Our AI-powered fintech development accelerates this maturation curve with pre-trained fraud detection models.

2025–2026 Trends in Money Transfer App Development

1. AI-Native Fraud Detection & Behavioral Biometrics

ML-based fraud scoring and behavioral biometrics (how users type and swipe) have moved from differentiators to baseline expectations. Apps without AI fraud infrastructure face growing losses and regulatory pressure in 2025.

2. Embedded Finance & Super-App Convergence

The line between remittance apps and broader financial platforms is dissolving. Designing your money transfer architecture modularly from day one so that savings, lending, or insurance can be added later without a rebuild. Our AI financial wellness app development is purpose-built for exactly this kind of expansion.

3. Open Banking API Expansion

Account-to-account transfers via open banking APIs are cheaper and more direct than card top-ups, and adoption is accelerating globally. It is driven by PSD2 in Europe and open banking frameworks in India, Australia, and Brazil.

4. Real-Time Payment Rails

Instant settlement is the new standard. FedNow and US RTP have expanded real-time domestic capacity; Project Nexus (BIS) is linking instant payment systems internationally. Money transfer apps built on batch-processing rails are already at a competitive disadvantage.

5. Blockchain & Stablecoin Settlement for Difficult Corridors

For high-cost corridors (US → Philippines, UK → Nigeria), stablecoin settlement on Stellar or Ripple's payment infrastructure offers meaningful cost and speed advantages. This is now an active cost reduction strategy that works.

Why Develop a Money Transfer App With Suffescom

- 13+ years in money transfer app development

- Expertise in secure, compliant fintech solutions

- KYC, AML, PSD2-ready implementations via our blockchain fintech solutions

- Scalable microservices-based architecture

- Fast launch with Agile development cycles

- Advanced security (AES-256, TLS 1.3, OAuth2)

- Seamless API & payment gateway integrations

- Custom-built solutions for P2P, remittance & B2B

- Cloud-native deployment (AWS, Google Cloud)

- Ongoing support and performance optimization

Conclusion

Money transfer applications represent a challenging yet fulfilling task for those developers who are able to incorporate compliance into the infrastructure of their products from day one, design their security protocols into the initial commits, pick the right technology stack according to scalability needs, and develop an intuitive user interface.

No matter what type of product you are developing, whether it’s a barebones peer-to-peer payments app, an international remittance service, or a customized enterprise solution for corporate payments, Suffescom can provide you with the expertise and experience necessary to succeed in such a demanding environment.

FAQs

1. How much time do we need to create a money transfer app?

The development process of such an application can be estimated at 4–9 months on average. For enterprise-level solutions that require multi-jurisdictional licenses, the process may take 12 to 18 months.

2. Is it possible to legally run money transfer apps?

Yes, you can, but in order to work in accordance with regulations, you will have to get proper authorization. Specifically, to launch an MTA in the USA, you should register as a money services business at FinCEN and acquire a money transmitter license for each state. In the European Union, you will have to comply with the PSD2 directive and acquire an EMI license.

3. What is the cost to develop a money transfer app?

The cost to develop a money transfer application depends on its features, complexity, and compliance requirements. A basic MVP typically starts from $25,000 to $35,000, while most mid-to-advanced solutions fall in the range of $25,000 to $75,000.

4. What technology stack is used to build money transfer apps?

The technology stack used in developing money transfer apps consists of components such as React Native or Flutter for mobile development, and React.js or Angular for web interfaces. On the backend, technologies like Node.js, Java (Spring Boot), or Python (Django/FastAPI) are used to handle APIs, business logic, and transaction processing.

5. Is it legal to build money transfer apps?

Yes, but you must comply with regional regulations. To build money transfer app solutions legally, you need licenses such as FinCEN MSB (USA), EMI license (EU), or RBI authorization (India), along with strict AML/KYC compliance.

6. What is the difference between a remittance app and a P2P payment app?

A remittance app development focuses on cross-border transfers with currency conversion and compliance, while P2P apps are designed for domestic, instant transfers between individuals with minimal fees.

7. How to develop a money transfer app?

The formula for building a successful money transfer application includes ensuring a user-friendly interface, high security, regulatory compliance, and scalability. These are some tips that help to keep your interface simple: provide fast and convenient transactions, and build strong integrations. Working with Suffescom will guarantee that your money transfer app will be successful.