Key takeaways:

- Financial systems today depend on integrated infrastructure that connects payments, core banking, compliance tools, and enterprise data platforms for seamless operations.

- AI adoption in financial services is accelerating, improving fraud detection, identity verification, and real-time decision-making across digital finance ecosystems.

- API-driven architecture enables secure and real-time communication between banking systems, ERP/CRM platforms, payment networks, and analytics engines.

- Key integration areas include payment processing systems, open banking frameworks, compliance and risk management tools, and core banking modernization.

- Event-driven and microservices-based architecture improves scalability, reduces system downtime, and supports high-volume financial transactions.

- A structured implementation lifecycle helps minimize operational risks while ensuring compliance with global financial regulations.

- Selecting a domain-specialized technology partner ensures secure, scalable, and regulation-ready financial infrastructure deployment

Want similar results? → Get a Free Quote

Fintech software integration is the process of connecting payment gateways, banking APIs, KYC/AML compliance engines, and enterprise platforms through a unified API architecture, enabling real-time data exchange, automated regulatory checks, and seamless transaction processing across your entire financial technology stack.

Today, the management of financial systems requires the use of various fragmented solutions like payment gateways, core banking, compliance systems, CRM, and analytics tools, which are unable to communicate with each other out of the box. This situation results in increased costs caused by the need to manually reconcile data between these platforms, delayed reporting processes, and long cycles of development and deployment of new products.

For banks, fintech startups, and enterprises building digital financial products, a well-structured integration architecture is no longer optional. It directly impacts transaction speed, regulatory compliance, system reliability, and customer experience in highly competitive financial markets.

Suffescom delivers end-to-end fintech integration architecture that connects every layer of your financial stack, from legacy core banking systems to modern embedded finance APIs — with PCI DSS compliance, real-time data flow, and 99.97% uptime built in from the ground up. Production-ready in 6 to 24 weeks depending on scope.

Fragmented Financial Systems Are Costing You More Than You Think

When your payment gateway, core banking platform, KYC engine, and ERP cannot communicate, the cost shows up everywhere in delayed settlements, compliance gaps, and missed product launches. Here are the four failure patterns we see most often in pre-integration fintech infrastructure:

Problem 1: Manual reconciliation consuming 40+ hours per week

Finance teams manually exporting and reconciling data between 4–8 disconnected platforms. This is a problem that disappears entirely with a properly architected integration layer, but until it is fixed, it compounds every week.

Problem 2: Compliance gaps from unsynchronised KYC/AML data

Regulators do not accept 'our systems were not connected' as an explanation for AML reporting gaps. Real-time compliance requires real-time data flow between identity verification, transaction monitoring, and regulatory reporting systems.

Problem 3: New product launches taking 12–18 months instead of 8 weeks

Every new financial product requires custom point-to-point integrations between the same systems. Without a unified API layer, development cycles never shorten; they accumulate technical debt with each new connection.

Problem 4: Transaction failures from latency between disconnected systems

Point-of-sale processing delays above 1.2 seconds erode payment approval rates and user trust. Production-grade fintech integration delivers sub-800ms end-to-end transaction processing by eliminating synchronous dependencies between services.

What Is Fintech Software Integration?

Fintech software integration is the process of connecting financial platforms, applications, data sources, and services to enable secure data exchange, workflow automation, and interoperability across your financial technology stack; exchange information and work on processes in a streamlined, secure, and consistent way. In its simplest form, a fintech integration solution means linking up a legacy core banking system with a new mobile app but also integrating a payment gateway, a fraud detection engine, a KYC identity validation tool, and a regulation reporting module in one financial technology stack.

At its simplest, it means linking a legacy core banking system to a modern mobile app. At its most complex, it means integrating a payment gateway, fraud detection engine, KYC identity validation tool, AML monitoring system, and regulatory reporting module into a single coherent architecture where every component communicates in real time.

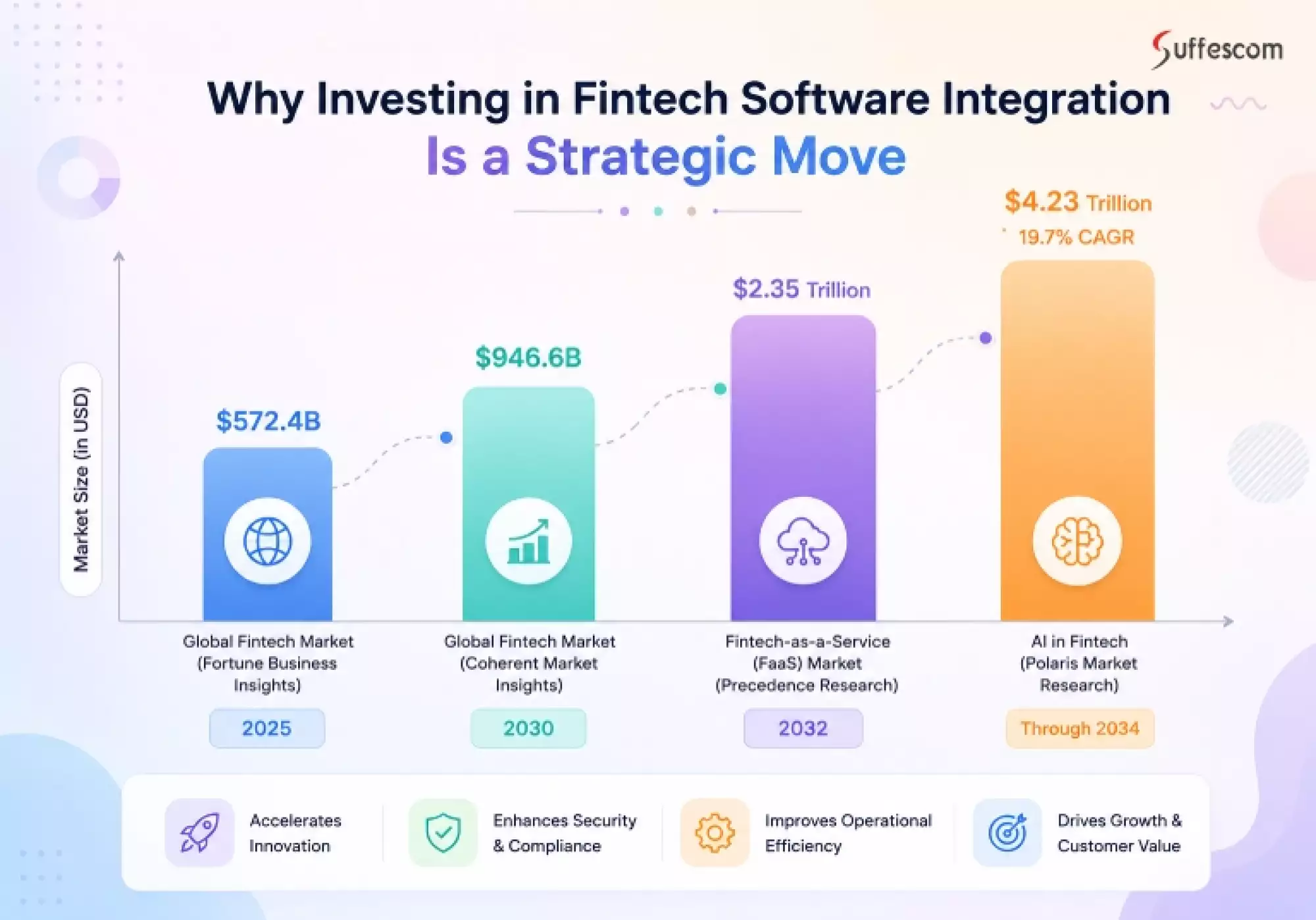

Why Investing in Fintech Software Is a Strategic Move

According to Fortune Business Insights, the global fintech market is valued at $340 billion in 2025 and projected to reach $460.76 billion by 2026, growing at an 18.2% CAGR through 2034.

Coherent Market Insights reports the fintech integration services market specifically will grow from $414.9 million in 2026 to $808.6 million by 2033, exhibiting a 10.0% CAGR.

The Fintech-as-a-Service (FaaS) market is expected to expand from $484.71 billion in 2026 to $1.82 trillion by 2035 at a 15.92% CAGR (Precedence Research).

The AI segment in fintech is projected to grow at 19.5% CAGR through 2034, making it the fastest-growing technology category (Polaris Market Research).

Companies that build integration architecture now capture compounding advantages: faster product launches, lower operational costs, stronger compliance posture, and better customer experiences — all at the same time.

Is Your Financial Ecosystem Struggling With Disconnected Systems

Streamline operations with a unified, API-driven fintech integration architecture that improves efficiency, data flow, and compliance readiness.

Key Components of a Production-Quality Fintech Integration Architecture

A production-ready fintech integration platform requires eight interdependent components working as a unified system:

API Gateway Tier

The centralized traffic management layer handling OAuth 2.0 and JWT authentication, rate limiting, API versioning, load balancing, and routing for all fintech API requests. Every external call enters and exits through this tier.

Core Banking Interface Adapter

Middleware that converts legacy COBOL and mainframe output into modern REST/JSON interfaces that contemporary fintech applications can process. This is what makes 40-year-old banking infrastructure compatible with 2026 mobile apps.

Event Stream

Apache Kafka or AWS EventBridge for asynchronous transaction event messaging between microservices — handling account movements, state changes, and transaction events without creating synchronous dependencies that become bottlenecks.

Identity & Compliance Adapter

Integrates KYC, AML, and eKYB verification services through secure API calls, enforcing regulatory requirements programmatically rather than manually.

Payments Gateway Adapter

Manages payment gateway integrations, card tokenization, 3D Secure 2.0 authentication, authorization workflows, and settlement processing across multiple payment rails.

Data Warehouse & Analytics

Aggregates transaction data from all integrated systems into a centralized layer for business intelligence, fraud pattern analysis, and regulatory compliance reporting.

Security & Encryption Tier

TLS 1.3 transport security, field-level encryption for personally identifiable information, HSM integration, and automated API key vault management.

Monitoring & Observability Tier

Distributed tracing via Jaeger or Zipkin, APM tools (Datadog, New Relic), financial transaction monitoring dashboards, and real-time SLA violation alerts.

Every Layer of Your Financial Stack, Connected

The right fintech integrations create a strong foundation for secure payments, workflow automation, regulatory compliance, and advanced AI Fintech App Development, enabling businesses to build scalable, intelligent, and future-ready financial ecosystems.

1. Core Banking Integration Services

Core banking integration is a process involving legacy banking systems such as Temenos, Finastra, Oracle FLEXCUBE, and Mambu connected to other fintech platforms. Such integration ensures secure real-time data flow, orchestration API, middleware implementation, and ISO 20022 messaging to upgrade banking processes with digital interoperability.

2. Payment Gateway Integration

Payment gateway integration provides a convenient means of transaction processing. Integrating fintech platforms with such processors as Stripe, Razorpay, Adyen, and PayU ensures secure transaction handling via key components, including PCI DSS compliance, tokenization, 3D Secure, webhook-based payments, fraud detection APIs, and chargeback management.

3. Open Banking API Integration

Integration with open banking is aimed at providing a secure exchange of financial data using standardized APIs in accordance with PSD2, OBIE, or RBI Account Aggregator regulations. Fintech API integration includes such processes as OAuth 2.0, consent management systems, account aggregation, and PIS integration.

4. KYC and AML Compliance Integration

Integration of KYC and AML compliance involves connections of the fintech software systems to API solutions for identity verification, sanctions databases, and risk management tools based on AI. The most sophisticated systems use such technologies as automated risk scoring, transaction monitoring, document validation, and fraud detection analytics.

5. Enterprise ERP and CRM Integration

Integration of enterprise fintech platforms involves connections with SAP S/4HANA, Salesforce, Oracle ERP, and Microsoft Dynamics 365 in order to automate financial reconciliation, general ledger synchronizations, invoice management, and customers' financial information management.

6. Digital Banking App Integration

The Digital Banking App connects various fintech services in a unified customer interface. The modern fintech architecture uses the Backend For Frontend solution, GraphQL APIs, microservices, and real-time data integration with banking systems, cards, lending, payments, and wealth management fintech services.

7. Embedded Finance Integration

Embedded finance integration connects payments, BNPL, lending, and insurance directly into your SaaS platform, e-commerce product, or logistics application using Banking-as-a-Service (BaaS) APIs. We integrate Railsbank, Treezor, Modulr, and other BaaS providers so your product becomes its own financial platform without building a bank.

The Suffescom 8-Layer Fintech Integration Stack

Every production-grade fintech integration Suffescom builds follows this architecture, eight interdependent layers working as a single, compliant, observable system. This framework was developed across 180+ client deployments and is the reason Suffescom integrations maintain 99.97% average uptime.

| Layer | Component | What It Does |

| Layer 1 | Client Layer | Mobile apps (iOS/Android), web dashboards, admin portals, and partner integrations — all entry points to the stack. |

| Layer 2 | API Gateway Tier | Kong or AWS API Gateway: OAuth 2.0/JWT auth, rate limiting, load balancing, API versioning, WAF, and DDoS protection. Every external call enters and exits through this layer. |

| Layer 3 | Core Banking Adapter | Middleware converting legacy COBOL/mainframe output into modern REST/JSON interfaces. Makes 40-year-old banking infrastructure compatible with current applications. |

| Layer 4 | Payment Gateway Adapter | Manages payment gateway integrations, card tokenization, 3D Secure 2.0, authorization workflows, and multi-rail settlement processing. |

| Layer 5 | Identity & Compliance Adapter | Integrates KYC, AML, and eKYB verification services via secure API calls. Enforces regulatory requirements programmatically at every transaction event. |

| Layer 6 | Event Stream | Apache Kafka or AWS EventBridge for asynchronous transaction event messaging between microservices — with dead-letter queues for guaranteed delivery. |

| Layer 7 | Data & Analytics | Aggregates transaction data for business intelligence, fraud pattern analysis, regulatory reporting, and real-time audit logging. |

| Layer 8 | Security & Observability | TLS 1.3, AES-256 field-level encryption, HSM integration, HashiCorp Vault, distributed tracing (Jaeger), APM (Datadog), and automated SLA alerting. |

How Leading Sectors Use Fintech Integration

| Industry | Key Integration Use Cases | Primary Regulations |

| Retail Banking | Real-time payment processing, account aggregation, AI fraud detection, open banking API exposure, digital KYC onboarding, mobile banking integration | PCI DSS, PSD2, GDPR, AML |

| Corporate & SME Banking | Multi-bank treasury management, automated bank-ERP reconciliation, supply chain finance APIs, trade finance automation, AI cash flow forecasting | Basel III, SOX, ISO 20022, SWIFT |

| InsurTech | Policy management integration, automated claims processing, telematics risk assessment, embedded insurance in fintech platforms, RegTech compliance | Solvency II, FCA, GDPR |

| WealthTech | Portfolio management integration, robo-advisor API connectivity, real-time market data feeds, tax optimisation tooling, alternative investment APIs | MiFID II, FCA, SEC |

| LendTech | Credit bureau API integration, alternative data scoring, automated loan origination, e-signature integration, instant payment disbursement | FCA, RBI, CFPB, GDPR |

| Payments & Remittance | Multi-rail payments, FX rate API integration, stablecoin payment gateways, ISO 20022 migration, merchant connections | PSD2, FATF, AML Directive |

API Protocol Selection for Fintech Integration: REST vs GraphQL vs gRPC vs WebSockets

| Protocol | Optimal Fintech Integration Use Case |

| REST (Representational State Transfer) | A stateless, HTTP-based protocol widely used in fintech software for payment APIs, open banking, and mobile fintech apps. Best for CRUD operations and scalable financial APIs. |

| GraphQL | Digital banking apps and fintech super apps requiring flexible, client-driven data queries — reduces over-fetching in financial dashboards |

| gRPC (Google Remote Procedure Call) | Low-latency, high-performance communication in trading platforms, fraud detection systems, and internal microservices |

| WebSockets & Webhooks | Real-time events — payment updates, transaction alerts, fraud monitoring, live price feeds |

| ISO 20022 & SWIFT APIs | Cross-border payments, banking interoperability, regulatory reporting, and enterprise fintech systems |

API Security Standards for Production Fintech Integration

Security isn't a feature to add before launch; it's a foundational requirement that must be embedded throughout the integration stack. A poorly secured financial API can expose customer PII, enable account fraud, violate PCI DSS and GDPR, and trigger regulatory penalties that dwarf development costs.

OAuth 2.0 With OIDC

The widely adopted standard for API access control and third-party authorization in open banking and fintech partnerships.

Mutual TLS (mTLS)

Certificate-based authentication for secure communications between API clients and servers, required in banking API integrations where both parties must prove identity.

API Key Lifecycle Automation

HashiCorp Vault, AWS Secrets Manager, or Azure Key Vault for automated key rotation without service downtime.

Rate Limiting and DDoS Mitigation

WAF and API gateway rules preventing credential stuffing, access abuse, and denial-of-service attacks.

Field-level Encryption

Encrypting financial data fields at the application layer, independent of transport encryption, narrows PCI DSS scope and protects data even if transport is compromised.

Payment Card Tokenization

Replacing card details with irreversible tokens for PCI DSS compliance and minimizing breach impact.

AI-based API Threat Detection

Behavioral pattern analysis across API transactions to identify account takeovers, injection attacks, and suspicious data extraction in real time.

How AI Is Reshaping Fintech Software Integration in 2026

Real-time Fraud Detection

Machine learning models analyze transaction patterns, device behavior, location data, and spending trends simultaneously, catching fraud in real time with significantly fewer false positives than rules-based systems.

Smart KYC/Document Validation

OCR, NLP, and computer vision automate identity and business verification, processing documents in seconds rather than days without manual review queues.

LLM-powered Financial Chatbots

Large language model-based assistants guide customers through account management, explain transaction history in plain language, and deliver personalized financial recommendations at scale.

Predictive Cash Flow and Credit Risk Scoring

AI-driven credit scoring models integrate alternative data sources — transaction history, behavioural patterns, and open banking data alongside traditional credit bureau data to produce more accurate risk assessments, particularly for thin-file borrowers who are underserved by traditional scoring methods.

Securing Trust Together: Fintech Integration Security Framework for Enterprises

Security must be embedded into the fintech integration stack throughout its entire existence, as any one bad link could make the transactions, data, or compliance processes vulnerable. Here are the basic principles that businesses should adhere to:

API Protection, Management, and Security

Businesses should protect their APIs using OAuth 2.0, JWT authentication, rate limiting, and other tools. Constant monitoring is necessary to prevent any misuse or unauthorized access.

Data Protection, Tokenization, and Encryption

All financial information should be encrypted both while being transferred (using TLS 1.2/1.3 protocols) and in storage (via AES-256). Tokenization replaces important data with tokens.

Identity and Fraud Prevention

KYC, AML, and KYB, along with machine learning-based fraud detection, allow for instant verification of the users' identity and prevention of suspicious transactions.

Audit Logging and Real-Time Monitoring

Centralized log storage, distributed tracing, and observability enable tracking of every transaction made for analysis and monitoring purposes.

Regulatory Compliance

PCI DSS, GDPR, ISO 27001, and PSD2 standards guarantee compliance and security.

The Suffescom 5-Phase Integration Framework

Successful financial software implementation requires a structured approach that balances speed, security, compliance, and seamless system integration.

Phase 1: Discovery and Architecture Design (Weeks 1-4)

- Audit of current financial systems infrastructure, data flows, integration interfaces, and technology debts

- Compliance mapping: determination of relevant standards (PCI DSS, GDPR, RBI, PSD2, MAS, SOX, DORA) and their technical requirements for implementation

- API landscape analysis: inventory of current APIs, identification of capability gaps, and target state architecture design for integration with technology choice justification

- Design of canonical financial data model: standardization of financial data models and definition of transformation rules from legacy to current systems

Phase 2: Integration Layer Development (Weeks 4-16)

- Configuration and setup of API Gateway (Kong, AWS API Gateway, Apigee, Azure API Management), including implementing authentication policies, rate limits, and routing.

- Creation of legacy adapter and connectors, such as IBM z/OS Mainframe connectors, FTP connectors, and SOAP to REST connector

- Message transformation using Apache Camel, MuleSoft, or custom ETL pipelines with idempotency considerations for financial transactions

- Installation of security setup, which includes an OAuth 2.0 authorization server, Mutual TLS certificates, and a secrets manager vault

- Set up and configuration of event streaming technology like a Kafka cluster with consumer groups and dead-letter queues.

Phase 3: Testing and Quality Assurance (Weeks 14-20)

- Integration testing: Testing data transformations, schemas, and business rules validation across all integration interfaces in the application

- Performance and load testing: High-load testing that exceeds 10,000 transactions per second, checks horizontal scalability, SLA on latency, and resource usage

- Penetration testing: API security testing, OWASP API Security Top 10, authorization bypass tests, and injection tests

- Compliance testing: Automated PCI DSS scanning, GDPR compliance for data flow management, audit logging, and regulatory reporting

- Chaos engineering and disaster recovery testing: Testing under failure, partitioning, and corruption scenarios

Phase 4: Production Deployment (Weeks 18-24)

- Blue-green deployment: Zero-downtime transition with instant rollback capability

- Canary releases: Staged traffic allocation (5% → 25% → 100%) to validate integration under production load before full cutover

- Monitoring stack activation: Distributed tracing, APM, financial transaction dashboards, automated SLA alerting

- Incident response runbooks: Documented procedures, on-call rotations, and automated resolution for common integration failures

Phase 5: Ongoing Optimization and Evolution (Month 6+)

- Lifecycle Management of API Versions: consumer communication, planning of deprecation cycles, managing backward compatibility periods, and supporting migrations.

- Performance Tuning: optimizing queries against the database, cache configurations, setting up CDNs, and scaling the infrastructure based on production traffic.

- Regulatory Change Management: adapting the integration layer for DORA, PSD3, FATF guidelines, and open banking architecture requirements.

- AI Model Governance: continuous retraining of AI models for fraud detection, credit risk assessment, and behavior analytics.

Fintech Integration Cost: What to Budget in 2026

Fintech integration costs range from $20,000 for a single payment gateway connection to $130,000+ for enterprise multi-system architecture. The right budget depends on five variables: number of systems to connect, applicable compliance standards, legacy system complexity, AI/automation requirements, and target geographic markets. Here is how scope maps to cost and timeline in practice.

Key Cost Drivers in Financial System Integration

| Cost Driver | Why It Matters | Estimated Cost Impact |

| Platform Features | Advanced capabilities like multi-currency payments, AI fraud detection, dashboards, and automation increase development effort. | $20,000–$55,000 |

| Compliance & Security | Implementing PCI DSS, KYC, AML, GDPR, encryption, and audit logs requires specialized expertise. | $15,000–$40,000 |

| Third-Party API Integrations | Banking APIs, payment processors, credit bureaus, and KYC vendors increase complexity. | $10,000–$35,000 |

| Legacy System Connectivity | Integrating old banking systems with modern fintech architecture requires middleware and custom APIs. | $25,000–$60,000 |

| AI & Automation Layer | Fraud detection, predictive analytics, smart underwriting, and document verification add cost. | $20,000–$50,000 |

| Infrastructure & Scalability | Cloud deployment, microservices, API gateways, and transaction scalability affect implementation. | $15,000–$35,000 |

Timeline and Budget by Project Scope

| Project Scope | Estimated Timeline | Estimated Cost |

| Basic Fintech Integration | 1–2 Months | $20,000–$40,000 |

| Mid-Level Platform Integration | 2–4 Months | $40,000–$75,000 |

| Advanced Fintech Integration | 4–6 Months | $75,000–$110,000 |

| Enterprise Fintech Solutions Integration | 6–8+ Months | $110,000–$130,000+ |

ROI Metrics

| ROI Driver | KPI to Measure | Business Outcome |

| Faster Go-to-Market | Product launch timeline | Faster revenue realization |

| Operational Efficiency | Reduction in manual workflows | Lower operational expenses |

| Fraud Prevention | Fraud detection accuracy | Reduced financial risk |

| Compliance Readiness | Audit issue reduction | Stronger regulatory confidence |

| Customer Retention | Transaction frequency & app engagement | Improved loyalty and LTV |

| Revenue Growth | Payment success & conversion rates | Increased profitability |

The Future of Fintech Platform Integration: What to Prepare for Now

As financial systems transform, developments in artificial intelligence, real-time payments, embedded finance, and regulation are rethinking the ways in which firms implement their fintech systems. The following are some trends that will shape the future of fintech:

1. Embedded Finance Becomes Mainstream

Services such as payments, lending, insurance, and BNPL (Buy Now Pay Later) are increasingly being embedded into e-commerce platforms, SaaS ecosystems, logistics solutions. Every software product is becoming a fintech product whether it plans to or not.

2. The Emergence of Real-Time Payment Platforms

New technologies such as UPI, FedNow, PIX, ISO 20022, and central bank digital currencies are revolutionizing the process of real-time payments, thus setting up the standard for instant transactions.

3. AI agents Automate Entire Workflows

Fraud detection, reconciliation, compliance reporting, and credit risk assessment are increasingly handled end-to-end by AI systems that operate faster and more accurately than manual processes.

4. Growth in Open Finance Ecosystem

Open finance not only enables users to access data on bank accounts but also information on investments, insurance, pensions, and credit cards.

5. Need for Compliance and Resilience

DORA, updated AML directives, and PSD3 are raising the bar for resilience and regulatory alignment. Integration architecture built to today's standards needs to be designed for tomorrow's requirements.

6. Blockchain and Tokenization of Financial Assets

Financial institutions are using smart contracts for settlements and tokenizing financial assets, creating new integration surface areas that API-first architectures need to support.

Why Businesses Choose Suffescom for Fintech Software Integration

As a trusted fintech software development company, Suffescom helps businesses build secure, compliant, and scalable fintech integrations tailored to modern financial ecosystems.

1. Fintech-specific Expertise in Software Development

We have deep fintech expertise in payment gateways, banking system integration, compliance automation, and API-driven architectures. This fintech-specific expertise ensures faster implementation, reduced integration risks, and more reliable system performance.

2. Security and Compliance

Financial software is usually exposed to various security risks. That is why you need to pay attention to fintech companies that have experience with PCI DSS, GDPR, SOC 2, AML, KYC, ISO 27001, and other regulatory requirements.

3. Integration Methodology

To ensure reliable fintech integration processes, consider choosing a fintech development partner with its proven approach to fintech platform integration, including discovery, architectural planning, development, testing, deployment, and monitoring phases.

4. Scalability-focused Expertise

At Suffescom, we build scalable fintech integration systems for UPI payment app development using AWS, Azure, GCP, API gateways, Kafka, and MuleSoft. This ensures high performance, resilience, and seamless business growth.

5. SLA-Backed Support

We provide SLA-backed support with continuous monitoring, proactive issue resolution, and performance optimization to ensure your fintech systems remain stable, secure, and high-performing post-deployment.

FAQs

1. What is fintech software integration?

Fintech software integration refers to the connection of various financial systems, payment gateways, banking platforms, and APIs that will allow for better data exchange and automation of processes. Fintech software integration is designed to make businesses work more efficiently and enhance their security.

2. Why is fintech platform integration important for businesses?

Fintech integration for business allows getting rid of silos in information, improving compliance, making operations more efficient, and speeding up transactions. Integration will help link payment systems, banking APIs, tools for fraud detection, and analytics platforms.

3. How long does fintech software integration take?

This process depends largely on the number of different components that need to be implemented. Payment gateway integration typically takes 4–8 weeks, while integration of enterprise fintech solutions may take several months (3–12 or even more).

4. What affects the cost of financial system integration?

It depends on many aspects like API complexity, necessary levels of security and compliance, need for third-party integrations, AI functionalities, etc. Fintech development cost should be taken into account.

5. Which compliance regulations govern fintech platform integration?

The most important ones include PCI DSS, GDPR, AML, KYC, PSD2, ISO 20022, and RBI Account Aggregator protocols. The compliance standards for software integration depend on the region, payment systems used, and financial services provided.

6. In what ways does AI benefit fintech software integration?

AI-powered fintech platform integration increases fraud prevention, automates customer identification procedures, performs advanced risk management assessments, and offers personalized financial interactions via prediction and automation techniques.

7. What are fintech API integration services?

These services involve integrating banking platforms, payment gateways, lending solutions, and other fintech-related applications using secure APIs for seamless real-time information exchange, transaction management, and financial interaction.

8. How can I pick the appropriate fintech software development partner?

You need to select the best fintech software development service that possesses proficiency in API integration, compliance regulations, payment systems, cloud-based architecture, and fintech security protocols.