The globe has switched to electronic money without making any fuss about it. Today, the process of paying for purchases with a mobile phone takes mere seconds compared to the time needed to stand in line at a bank counter. The key to each seamless digital payment lies in a well-designed payment application that is fast, secure, and user-friendly.

This guide is a must-read for startup owners, product managers at enterprises, and entrepreneurs interested in payment software development. Here, you will learn what a payment app is, its cost, the correct development process, and the importance of selecting the right payment application development company.

The Digital Payment Revolution Is Already Here

The numbers don't lie: digital payments are the foundation of global commerce.

According to Coinlaw, the global digital payments market will process $26.89 trillion in transactions in 2026, an 11.73% increase year-over-year.

5.2 billion people worldwide will use digital wallets by 2026; that's over 60% of the global population.

Digital wallets captured 53% of all global online purchases in 2025, more than double the share of credit cards.

The digital payments market size stands at USD 145.03 billion in 2026 and is projected to reach USD 351.07 billion by 2031, reflecting a 19.34% CAGR for the forecast period - Mordor Intelligence

86% of global consumers now use contactless payment methods, a behavior that is becoming permanent.

Real-time payment transactions are on track to hit 428 billion annually by 2026, with India's UPI holding 49% of global volume.

What Is Payment App Development?

Payment app development entails the creation of a mobile or online platform that allows the user to conduct payment activities, including sending and receiving funds. This goes beyond just developing the transferring screen; it includes payment gateway integration, banking API integrations, the creation of an anti-fraud framework, compliance such as PCI DSS and KYC/AML regulations, and the UX component that builds trust through each step.

Creating a payment platform requires merging fintech engineering, security architecture, and design principles. A robust payment platform connects users' bank accounts or cards to a digital interface where transactions occur in real-time with instant confirmation.

How a Payment Application Works: Technical Flow

Before you develop a payment application, you need to understand the transaction flow:

- Transactions initiated by users using the application interface (using taps, QR code, or manual input).

- The application collects the transaction and authenticates the user using PIN or biometric identification.

- Raw card information or account details are not stored in any local device but rather through tokenization of data.

- The encrypted transaction is forwarded to the payment gateway, which connects with the acquiring bank.

- Further, the request is passed on to the card network, such as Visa/MasterCard/RuPay.

- The issuing bank processes the transaction based on balance verification and risks of fraud, either approving or declining.

- The response is relayed back through the same process and reflected within the application.

Technical Insight

Modern payment apps using tokenization (PCI DSS Token Service Providers) and TLS 1.3 encryption ensure that even if data is intercepted in transit, it remains unreadable. Zero-trust architecture adds a layer by verifying every access request regardless of origin.

Build a Secure & Scalable Payment Application

Collaborate with our experts to design and launch a high-performance payment solution tailored to your business goals.

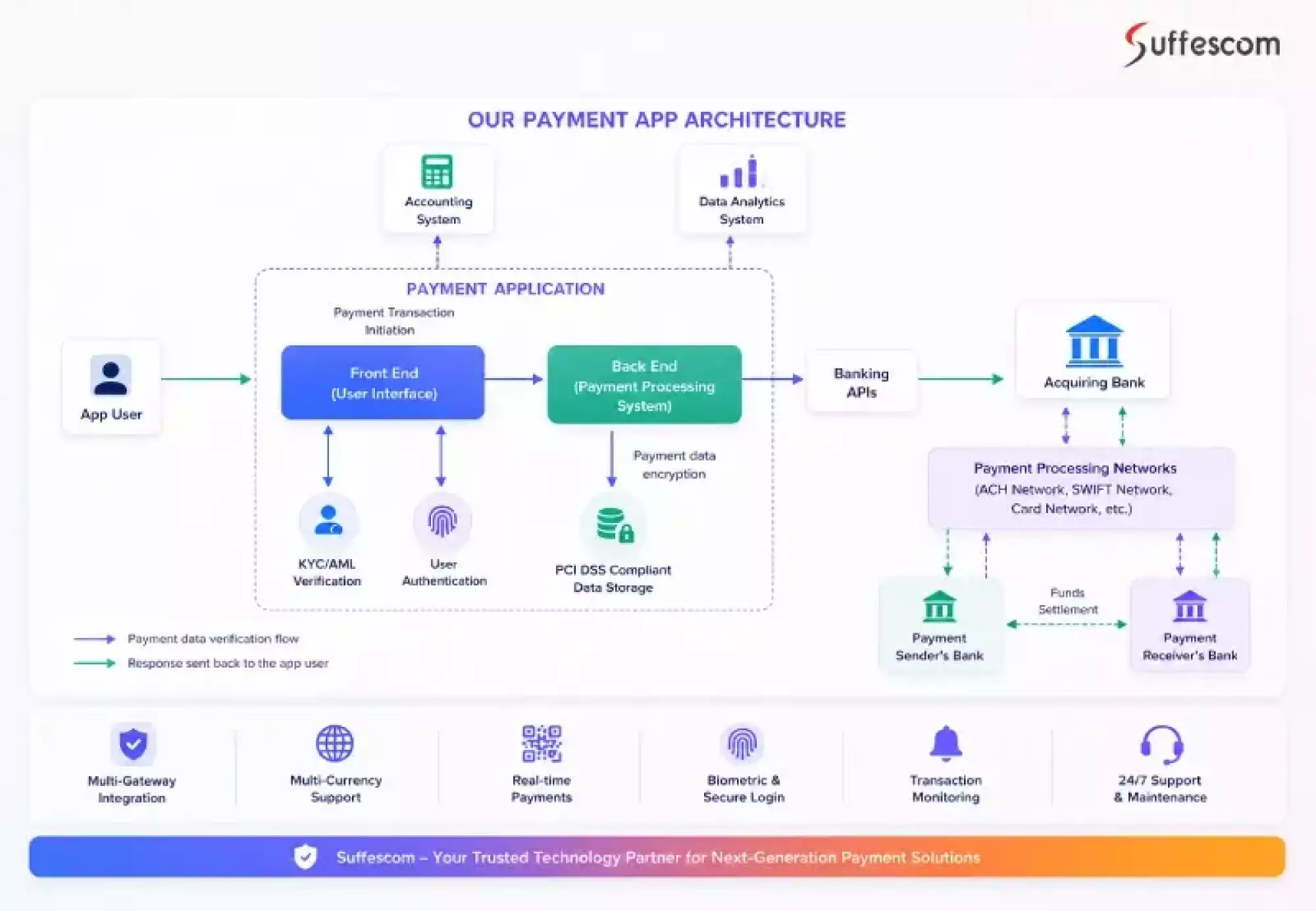

Payment App Development Architecture

At Suffescom, payment app development is built on a secure, API-driven architecture that ensures seamless, real-time transaction processing with full regulatory compliance.

How the System Works

Users initiate transactions through a secure front-end interface, supported by KYC/AML verification and authentication layers. The request is processed by a robust backend system that handles validation, routing, and payment orchestration.

Secure Processing & Integrations

This architecture also supports seamless fintech integration service capabilities, allowing businesses to connect payment ecosystems, banking infrastructure, and third-party financial tools through secure APIs.

Data & Intelligence Layer

Transaction data flows into analytics and accounting systems for real-time reporting, reconciliation, and performance tracking.

What This Means for You

This architecture ensures high scalability, low-latency processing, and secure financial operations, delivering reliable and future-ready payment applications.

Types of Payment Applications You Can Build

Before your payment application development company writes a single line of code, you need to decide which payment model you are building. Each type serves a different market, requires different compliance, and generates revenue differently.

1. P2P Payments Apps

This solution enables users to pay money from one individual to another person via mobile phones. There are no intermediaries involved, just quick, convenient, and hassle-free payments. Venmo, Cash App, and Zelle are all P2P payment apps that you've probably heard of. When you develop a peer-to-peer payment app, you will be able to make quick money transfers without having to deal with bank queues or extra documentation.

2. Mobile Wallets (eWallet) Apps

Such apps store your debit/credit cards' details in order to make payments either through contactless payments enabled with NFC technology or QR code-based transactions at the checkout point. Apple Pay, Google Wallet, and Samsung Pay are some examples of eWallet applications. The development process will require the use of NFC technology, payment tokenization, and strict SDK implementation.

3. Merchant Payment Apps

Merchant payment apps are point-of-sale solutions used by businesses to process customer payments. These integrate directly with payment gateways and handle card-present transactions. Square and Stripe Terminal operate in this space. Payment software development for merchants requires real-time transaction processing, receipt generation, and inventory integration.

4. Bank-Based Payment Apps

Developed by traditional banks and Neobanks, these apps implement standard banking infrastructure on a digital interface. They are highly regulated, deeply trusted, and integrate directly with core banking systems. Examples include Chase Mobile, Bank of America, and most neobank offerings.

5. BNPL & Payment App Lenders

The Buy Now, Pay Later approach involves making loans to consumers based on the credit decision and subsequent processing and managing installments made by the lender. This is the most regulation-heavy category in payment application development, requiring AML compliance, credit risk models, and multi-jurisdiction licensing.

6. Cross-Border / Remittance Payment Apps

Apps enabling international money transfers must handle multiple currencies, FX conversion APIs, SWIFT/SEPA integration, and strict AML/KYC compliance. If you’re exploring how to create a money transfer app, this category requires advanced architecture and regulatory readiness due to its high technical complexity.

Regional Payment Ecosystem Considerations for Global Apps

When you develop a payment application for multiple markets, regional payment rails, regulatory frameworks, and settlement timelines directly impact your architecture, compliance scope, and user experience.

| Region | Key Payment Methods | Regulatory Framework | Settlement Time |

| United States | ACH, card networks, Zelle | State Money Transmitter Licenses, FinCEN, CFPB | 1–3 business days (ACH) |

| Europe | SEPA Instant, cards, Open Banking | PSD2, GDPR, EMI licensing | Instant (SEPA Instant) |

| India | UPI, RuPay, IMPS | RBI guidelines, NPCI rules | Real-time (UPI) |

| Latin America | PIX (Brazil), SPEI (Mexico) | Local central bank regulations | Real-time |

| Southeast Asia | GrabPay, GCash, local wallets | Country-specific regulations | 1–2 days |

What Features Should a Payment App Have?

User Registration & KYC Onboarding

Secure onboarding with identity verification APIs, enabling fast KYC completion, regulatory compliance, and trusted user activation from the first signup.

Multi-Factor Authentication (MFA)

Layered authentication using OTP, biometrics, and time-based codes to ensure strong account security and reduce fraud risks in payment systems.

Instant Fund Transfers

Real-time money movement via modern payment rails such as RTP, UPI, and SEPA Instant, enabling seamless and low-latency transactions across networks.

Payment Gateway Integration

Unified integration with leading gateways like Stripe, Adyen, and Razorpay to process secure, scalable, and global digital transactions.

Digital Wallet & Balance Management

Secure wallet infrastructure with encrypted ledgers and escrow capabilities for storing, managing, and transferring digital funds efficiently.

Transaction History & Analytics Dashboard

Real-time visibility of all transactions with structured reporting, filtering, and analytics for improved financial tracking and transparency.

QR Code Payments

Contactless payment system powered by dynamic QR generation for fast peer-to-peer and in-store transactions.

Push Notifications & Alerts

Instant transaction updates and security alerts are delivered through real-time notification systems for better user engagement and control.

Tokenization & Data Security Layer

Sensitive card data is replaced with secure tokens using PCI-compliant systems, reducing exposure to fraud and data breaches.

PCI DSS Compliance Framework

Built-in compliance architecture ensures secure payment processing, audit readiness, and adherence to global financial security standards.

Advanced Features That Drive Competitive Advantage

After validating your MVP, these advanced features elevate your payment application from being just another payment app to becoming the best in the market:

Fraud Prevention via Real-Time Machine Learning Models

Your models monitor transactions in real-time, recognizing anomalies and unusual spending patterns, as well as any unauthorized activity. By 2026, you can no longer offer an app with machine learning algorithms that predict fraudulent transactions; they are expected. Consider adding a risk score engine (TensorFlow Lite for on-device computation or cloud-based systems such as Sardine or Featurespace) to ensure user and company safety.

Biometrics Verification (Face ID, Fingerprint, Liveness Detection)

A password alone no longer guarantees security. You need to add face ID or fingerprint authentication methods and implement behavioral analysis. With liveness detection, you prevent any potential spoofing attacks. Your customers will appreciate it since this feature is more than security; it also serves as a trust indicator.

In-App Card Issuance and Virtual Cards

Consider integrating your product with Banking-as-a-Service companies such as Marqeta, Lithic, or Stripe Issuing and enabling your users to create virtual cards directly from the application.

Payments, Invoicing & Subscriptions

In the case of B2B payment systems and SaaS payment apps, invoicing and subscriptions ensure regular transactions for the app. The users can create invoices, request payment, monitor transactions, and pay their bills. Subscription models need idempotent APIs to avoid duplicate billing.

Open Banking API Implementation

The open banking protocols (PSD2 in Europe, Open Banking in the UK, future standardization in the USA) enable payment apps to access the bank account information of their users. With this technology, apps can facilitate account-to-account transfers, analyze the cash flows, and provide personalized financial advice while avoiding card network fees.

Split Payments & Group Expense Management

Group expenses ranging from vacations to lunches can be easily managed and shared using inbuilt split payment facilities within the payment apps. It makes the app more user-friendly and helps it gain traction through word-of-mouth.

Multi-Currency Support & Foreign Exchange Conversion

A must-have feature when targeting the international market. Payment apps should incorporate real-time foreign exchange rate data from providers such as Open Exchange Rates or Wise Business API to convert currency amounts for the users beforehand.

AI-Powered Spending Analytics & Budgeting

Categorize transactions automatically using NLP-based merchant classification. Provide users with spending insights, budget alerts, and financial health scores. This feature increases app stickiness, reduces churn, and supports premium subscription monetization.

How to Differentiate Your Payment App in a Competitive Market

To stand out in modern payment app development, you need more than standard features; differentiation comes from performance, UX, and value-added capabilities.

- Vertical Specialization: Industry-focused solutions (healthcare payments, gig payouts, SMB invoicing)

- Superior UX/UI: One-tap payments, voice-enabled actions, accessibility-first design

- Lower Transaction Costs: Optimized fee structures and zero-cost instant transfers

- Faster Settlement: Real-time processing and instant balance updates

- Advanced Security: Behavioral biometrics and fraud risk scoring engines

- Financial Intelligence: AI-driven spending insights, auto-savings, credit tracking

- Social Payments: Activity feeds, bill splitting, and group expense management

- Business Capabilities: Invoicing, subscriptions, and multi-user account controls

- Global Readiness: Multi-currency wallets and cross-border payment support

- Loyalty Systems: Cashback, rewards, and merchant-driven incentive programs

Strategic Benefits of Payment App Development for Scalable Fintech Growth

Building a secure and scalable payment application delivers measurable advantages across speed, compliance, and business growth. If you are planning how to create a payment app, these benefits highlight why an iterative and compliant development approach ensures faster launch and higher ROI.

Quick and Agile Project Execution

Quick start of the project in 1-2 weeks using agile sprints and DevOps delivery pipelines for delivering continuously and accelerating time to market.

Regulatory-Compliant Solution

In-built compliance with regulatory requirements like PCI DSS, 3D Secure, AML/KYC, GDPR, PSD2, and CCPA for safe and reliable payments ecosystem worldwide.

Transparency in Project Execution

Key performance indicators and regular progress monitoring and reporting guarantee full transparency, accountability, and delivery quality.

Quick ROI Through Delivery Approach

Focus on essential features in an incremental and iterative manner for early deployment and fast ROI.

How to Build a Payment App: Step-by-Step Development Process

Creating an app for payments involves following a systematic development process comprising various phases. The main cause of why many fintech ventures exceed budgets or do not launch successfully lies in skipping key phases such as discovery or planning compliance. Below you can find the step-by-step process in creating an app for payments:

Phase 1: Discovery, Market Research & Compliance Roadmap

Every effective payment application begins with clarity. Who is your target audience? What problem are you solving? Which legal frameworks apply to your business? This phase leads to:

- Requirements specifications for each app function, including user account creation and transactions

- Personas and journey maps for your primary target audiences

- Compliance roadmap: necessary compliance certification, their timeline (e.g., PCI DSS, PSD2, EMI licensing, Money Transmitter license)

- Technical architecture: database, API integration, cloud computing, etc.

- Competitive gap assessment: what competitors' apps do not have but yours will offer

- This phase takes about 10% of your total budget but solves 50% of your future problems.

Phase 2: User Interface/User Experience Design and Prototypes

The most technologically advanced payment application is doomed to failure if it’s not intuitive. In design, it’s imperative to focus on simplicity and trust, which are traits that can be difficult to accomplish when designing financial applications.

- Wireframes showing how the basic flow of the application works, without the inclusion of any graphical elements

- Interactive prototype that can be reviewed by stakeholders before any coding has begun

- Fully developed user interface design that adheres to standards of accessibility (WCAG 2.1) and follows guidelines for iOS and Android operating systems

- All payment workflows mapped from start to finish, including error handling processes

- Security architecture documentation, including fraud detection workflows

Phase 3: Technology Stack Selection

The right technology stack balances performance, security, scalability, and developer availability. Here is the recommended stack for modern payment app development:

Payment App Development Technology Stack (2026)

| Layer | Recommended Technologies | Why |

| Frontend (iOS) | Swift, SwiftUI | Native performance with full Apple Pay SDK integration for seamless iOS payment experiences |

| Frontend (Android) | Kotlin, Jetpack Compose | Optimized native performance with direct Google Pay and Android ecosystem support |

| Cross-Platform | Flutter (46% market share in 2026) | Single codebase with near-native performance, reducing development time and cost |

| Backend | Node.js, Python (Django/FastAPI), Java (Spring Boot) | High scalability and efficient asynchronous transaction processing for payment systems |

| Database | PostgreSQL (ACID-compliant) | Ensures financial-grade data integrity and reliable transaction consistency |

| Cache Layer | Redis | Improves session handling, rate limiting, and real-time transaction speed |

| Message Queue | Apache Kafka / RabbitMQ | Enables asynchronous payment processing and event-driven architecture |

| Cloud Infrastructure | AWS (Fargate, RDS, KMS), GCP, Azure | Provides auto-scaling, high availability, and enterprise-grade compliance support |

| Payment Gateway | Stripe, Adyen, Braintree, Razorpay | Secure transaction processing with built-in PCI DSS compliance |

| Banking APIs | Plaid, Dwolla, Finicity, Open Banking APIs | Enables secure bank account linking and financial data connectivity |

| KYC / Identity Verification | Onfido, Jumio, Persona | Automates identity verification for regulatory compliance and fraud prevention |

| Fraud Detection | Sardine, Featurespace, Stripe Radar | AI/ML-powered risk scoring to detect and prevent fraudulent transactions |

| Encryption | AES-256 (at rest), TLS 1.3 (in transit) | Industry-standard financial data protection ensuring end-to-end security |

Phase 4: Backend Development & API Integration

The backend is the financial engine of your payment application. Transactions, user authentication, wallet balance updates, and audit trails for regulatory compliance are all handled there. Important engineering activities include:

- Developing RESTful/GraphQL APIs with proper client-server communication and strict input validation

- Idempotence handling for avoiding duplicated transactions

- Introducing payment processor APIs (Stripe, Adyen) that manage card data security under the PCI DSS

- Constructing an immutable ledger system: all debits and credits have to be registered with timestamps and transaction IDs

- Banking APIs integration (Plaid, Open Banking): for verifying accounts and getting balances

- Event-driven architecture with message queueing: for asynchronous transactions

- Admin dashboards with transaction monitoring and dispute resolution features

Phase 5: Security Implementation

Security in the payment app development process isn't something you implement later — it is the architectural foundation that will hold your project up. You are going to process your users' payments and collect their sensitive financial information.

- Important Security Solutions for Your Payment Application

- End-to-end encryption: TLS 1.3 for transferring the data and AES-256 for storage — service providers don't have access to the raw sensitive information

- Multi-factor authentication (MFA): biometrics + device binding + behavioral analytics

- Zero-trust architecture: every access request is verified regardless of origin or previous session

- Real-time transaction monitoring with ML-based anomaly detection

- Penetration testing: $5,000–$30,000 per audit, mandatory before launch and annually thereafter

- Secure key management using cloud KMS (AWS KMS, Google Cloud KMS)

- Rate limiting and DDoS protection at the API gateway layer

Phase 6: Compliance & Regulatory Integration

Regulatory compliance is not optional. It is the gateway to operating legally in financial services. Requirements vary significantly by region and payment model:

Payment App Development Compliance & Regulatory Requirements (2026)

| Regulation | Applies To | Requirement |

| PCI DSS (Level 1–4) | Any app processing card payments | Mandatory compliance; partially managed through certified payment gateways |

| KYC (Know Your Customer) | All money transmission apps | User identity verification to prevent fraud and ensure regulatory compliance |

| AML (Anti-Money Laundering) | Money transmitters, digital wallets | Continuous transaction monitoring and suspicious activity reporting |

| GDPR | Apps serving EU users | Data protection, user consent management, and right to data erasure |

| CCPA | Apps serving California users | Data privacy rights, transparency, and opt-out mechanisms |

| PSD2 / Open Banking | EU/UK payment applications | Strong Customer Authentication (SCA) and secure API access requirements |

| SOC 2 Type II | B2B payment platforms | Audit for security, availability, and processing integrity controls |

| Money Transmitter License | US-based P2P and wallet apps | State-level licensing requirements (most US states mandate compliance) |

Phase 7: Testing Strategy for Payment Applications

Payment apps require more rigorous testing than standard applications because errors involve real money and regulatory liability. Never launch without completing all testing phases:

- Functional Testing: Verifies every feature works correctly across scenarios and edge cases (failed payments, network drops mid-transaction, duplicate submission attempts)

- Security Testing: Penetration testing, OWASP Top 10 vulnerability assessment, code analysis, and infrastructure security review

- Performance Testing: Ensures the app handles expected transaction volumes — load test to 10x your peak projection

- Compliance Testing: Verifies adherence to PCI DSS requirements and app store payment guidelines

- Integration Testing: Every API endpoint — payment gateway, banking API, KYC service — tested independently and in combination

- UAT (User Acceptance Testing): Real users complete real payment scenarios before release

Phase 8: Launch, App Store Submission & Post-Launch

Launching a payment app involves considerations beyond standard app releases. Payment apps face additional scrutiny during App Store review:

- Complete all regulatory filings and obtain necessary financial licenses before submission

- Ensure privacy policy and terms of service have been reviewed by financial services legal counsel

- Deploy fraud monitoring systems — they must be staffed and operational before go-live

- Set up customer support processes specifically for payment disputes and failed transactions

- Configure real-time alerting for transaction anomalies, error rate spikes, and security events

- Plan a phased rollout: beta launch to a limited user segment before full public release

Launch Your Payment App with Confidence

From architecture to compliance, we help you develop a reliable payment ecosystem that drives growth and user trust.

How Much Does It Cost to Build a Payment App in 2026?

Understanding these variables helps businesses accurately estimate budgets and make informed decisions when planning to develop a payment application that is secure, scalable, and future-ready.

Payment App Development Cost & Timeline Breakdown

| Tier | Description | Cost Range | Timeline |

| Basic MVP | Single platform, 1 transaction type, basic security, minimal compliance | $20,000 – $60,000 | 2–4 months |

| Standard App | iOS + Android, multi-payment types, full KYC, PCI DSS compliance, gateway integration | $60,000 – $80,000 | 4–8 months |

| Full-Featured Platform | Multi-platform, AI fraud detection, biometrics, multi-jurisdiction compliance, analytics | $80,000 – $1,00,000+ | 8–14 months |

| Enterprise Payment System | Banking-grade infrastructure, BaaS integration, multi-market support, custom ledger system | $1,00,000 – $1,20,000+ | 12–24 months |

Cost Breakdown by Development Phase

Understanding how the budget is distributed across phases helps you prioritize spending and avoid surprises:

Payment App Development Cost Allocation by Phase

| Phase | % of Total Budget | What It Covers |

| Discovery & Strategy | 10% | Market research, compliance roadmap, technical architecture, SRS documentation |

| UI/UX Design | 15–25% | Wireframes, interactive prototypes, high-fidelity UI design, accessibility compliance |

| Backend Development | 30% | APIs, database design, server-side infrastructure, payment gateway integration |

| Frontend Development | 20% | iOS, Android, or cross-platform app development with full feature implementation |

| Security & Compliance | 10% | Penetration testing, PCI DSS implementation, encryption setup, and regulatory compliance |

| QA & Testing | 15% | Functional testing, security testing, performance validation, integration testing |

| Deployment & Launch | 10% | App store deployment, cloud configuration, monitoring and production setup |

| Annual Maintenance | 15–25% of initial cost/year | Bug fixes, OS updates, feature enhancements, security patches and system upgrades |

Security & Compliance in Payment Application Development

Security and compliance form the core of every payment application, guiding how systems are designed, developed, and deployed. A well-structured approach ensures secure transactions, protects user data, and builds long-term trust while meeting all necessary regulatory standards.

PCI DSS Compliance: What It Means for Your App

Every business accepting card payments must comply with the Payment Card Industry Data Security Standard (PCI DSS), regardless of transaction volume, geography, or integration method. PCI DSS compliance has four merchant levels based on annual transaction volume, with Level 1 (6M+ transactions) requiring the most rigorous annual audits.

The most cost-effective approach for new payment app development is to use a PCI-certified payment gateway (Stripe, Adyen, Braintree). These providers absorb the card data storage and processing compliance burden, reducing your PCI DSS scope significantly.

KYC/AML: Identity Verification Architecture

Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements mean your payment application must verify user identities before allowing financial transactions. Modern KYC implementation uses automated identity verification APIs (Onfido, Jumio, Persona) that perform:

- Government ID document verification (passport, driver's license, national ID)

- Liveness detection to prevent spoofing with static images

- Database checks against sanctions lists, PEP (Politically Exposed Persons) databases, and adverse media

- Ongoing transaction monitoring for AML patterns post-onboarding

Security & Compliance in Payment Application Development

Security and compliance form the core of every payment application, guiding how systems are designed, developed, and deployed. A well-structured approach ensures secure transactions, protects user data, and builds long-term trust while meeting all necessary regulatory standards.

PCI DSS Compliance: What It Means for Your App

Every business accepting card payments must comply with the Payment Card Industry Data Security Standard (PCI DSS), regardless of transaction volume, geography, or integration method. PCI DSS compliance has four merchant levels based on annual transaction volume, with Level 1 (6M+ transactions) requiring the most rigorous annual audits.

The most cost-effective approach for new payment app development is to use a PCI-certified payment gateway (Stripe, Adyen, Braintree). These providers absorb the card data storage and processing compliance burden, reducing your PCI DSS scope significantly.

KYC/AML: Identity Verification Architecture

Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements mean your payment application must verify user identities before allowing financial transactions. Modern KYC implementation uses automated identity verification APIs (Onfido, Jumio, Persona) that perform:

- Government ID document verification (passport, driver's license, national ID)

- Liveness Detection to Prevent Spoofing With Static Images

- Database checks against sanctions lists, PEP (Politically Exposed Persons) databases, and adverse media

- Ongoing transaction monitoring for AML patterns post-onboarding

How Payment Apps Generate Revenue: Monetization Models

Choosing the right monetization strategy ensures sustainable growth and maximizes profitability when you develop a payment application. These are the primary monetization frameworks used by successful payment platforms today:

Transaction Fees (Most Common) Charge a small percentage (0.5%–3%) or a flat fee per transaction processed. This is the model used by Stripe, Square, and most payment gateways. It scales directly with volume and requires no upfront cost to users, which accelerates adoption.

Subscription / SaaS Plans Offer tiered monthly plans for businesses that covers transaction limits, API access, advanced analytics, or priority support. Ideal for B2B payment platforms and merchant-facing tools.

Currency Conversion Spread For cross-border and remittance apps, generate revenue on the foreign exchange rate spread. Wise pioneered transparent FX pricing; your differentiator can be competitive rates with better UX.

Interchange Revenue (Card Issuing) Partner with a BaaS provider such as Marqeta or Stripe Issuing to issue virtual or physical cards. You earn a portion of interchange fees each time your card is used for a purchase.

Premium Features (Freemium) Offer a free base tier with limitations and charge for premium features — higher transfer limits, instant payouts, advanced reporting, or white-label options for business accounts.

Interest on Stored Balances. If your platform holds user funds in an escrow or wallet structure, you can earn interest on pooled balances. This requires appropriate licensing — consult your fintech compliance roadmap early.

BNPL Interest & Late Fees For Buy Now Pay Later platforms, revenue comes from merchant discount rates, consumer interest on extended plans, and late fees, regulated carefully by jurisdiction.

Payment App Development Trends Shaping the Future of Digital Payments

The payment technology landscape is evolving faster than ever. These are the trends actively shaping what users expect and what developers are building:

1. Native Fraud Protection & Personalization

In-device machine learning models can be used for immediate fraud score analysis, transaction categorization via NLP, and cash flow predictions, complying with all rules related to explainable AI technologies.

2. Embedded Financial Services & Invisible Payments

Invisible payments are possible due to the integration of payments within platforms with the help of an API-driven approach and whitelabel components and compliance layers.

3. Open Banking & Account-to-Account Payments

Account-to-account payments via Open Banking APIs reduce reliance on card networks by lowering processing costs and enabling faster settlement cycles.

4. Blockchain Payment Infrastructure & Stablecoins

Blockchain networks facilitate near-instantaneous cross-border settlements, whereas stablecoins offer low volatility and fast business-to-business payments.

5. Continuous Biometric & Passive Authentication

Biometric and passive continuous verification based on device behavior analysis (device movement and typing patterns) improves security without hindering users' actions.

6. Real-Time Payment System (RTP)

FedNow, UPI, and SEPA Instant infrastructure enable instant payment processing, replacing traditional batch systems, making real-time capabilities essential in modern UPI payment app development.

7. CBDC Integration & Wallet Interoperability

Central Bank Digital Currencies will drive mandatory support for sovereign digital cash systems, requiring wallet-level integration, compliance with monetary policy frameworks, and real-time settlement compatibility across regulated payment networks.

8. ISO 20022 Messaging Standard Adoption

Migration to ISO 20022 enables structured, high-fidelity financial data exchange, improving interoperability between banking systems, enhancing transaction metadata depth, and supporting advanced compliance, analytics, and cross-border payment reconciliation.

9. Quantum-Resistant Cryptographic Migration

Next-generation payment infrastructure will transition toward post-quantum encryption algorithms to mitigate risks from quantum computing threats, ensuring long-term security of transaction layers, key exchange mechanisms, and digital identity protection systems.

Transform Your Payment Idea into a Live Product

Turn your concept into a fully functional, secure, and scalable payment application with expert guidance.

Why Businesses Choose Suffescom for Payment App Development

- 13+ years in fintech software development from lean P2P MVPs to enterprise-grade banking platforms.

- 250+ in-house fintech experts, such as developers, security architects, compliance specialists, and UX designers, working under one roof, not outsourced.

- Dedicated compliance practice to navigate PCI DSS, KYC/AML, GDPR, PSD2, and Money Transmitter Licensing requirements across 25+ countries that is built into the project plan from Day 1, not bolted on at the end.

- Full-spectrum payment app portfolio from P2P payment apps and UPI solutions to BNPL platforms, and white-label digital banking, we have delivered every payment app category.

- Security-first engineering with penetration testing, AES-256 encryption, zero-trust architecture, and ML-based fraud detection integrated at the architecture layer, not as an afterthought.

- 4.8+ star rating across Clutch, G2, DesignRush, and Trustpilot backed by 200+ successfully delivered projects across fintech, blockchain, and digital payments.

- Agile delivery with full transparency, sprint-based execution, weekly reporting, and a dedicated project manager from kickoff to post-launch maintenance.

Our Proven Payment Application Development Success Stories

TransloPay

Cross-Border Payment Platform for Global Transfers

TransloPay facilitates multi-currency transactions with real-time FX conversion and seamless international transfers. It integrates with SWIFT and SEPA networks while ensuring AML/KYC compliance across regions. The cloud-native infrastructure supports high transaction volumes with fast and reliable settlements.

View Case Study

FAQs

1. What is payment app development?

Payment app development is the process of building digital platforms that enable secure money transfers, wallet management, and payment processing using APIs, encryption, and banking integrations.

2. How to create a payment app from scratch?

To create a payment app, you need to define requirements, design UI/UX, build backend architecture, integrate payment gateways, implement security layers, and ensure regulatory compliance before deployment.

3. What are the key features of a payment application?

Core features include digital wallets, instant transfers, multi-currency support, KYC verification, QR payments, transaction history, fraud detection, and secure authentication systems.

4. How much does it cost to develop a payment application?

The cost typically ranges from $20,000 for a basic MVP to $1,20,000+ for a full-scale fintech platform, depending on features, compliance, and technology stack.

5. How secure are modern payment applications?

Modern payment apps use AES-256 encryption, tokenization, MFA, and AI-based fraud detection systems to ensure secure and compliant financial transactions.

6. Can a payment app support multiple currencies and countries?

Yes, advanced payment applications support multi-currency wallets, FX conversion APIs, and cross-border payment systems for global financial operations.

7. What technologies are used in payment app development?

Common technologies include Node.js, Java, Flutter, PostgreSQL, Redis, Kafka, cloud platforms like AWS, and APIs from Stripe, Adyen, or Razorpay.

8. Do payment apps require legal compliance?

Yes, payment apps must comply with PCI DSS, KYC/AML regulations, GDPR, PSD2, and in some cases, obtain Money Transmitter Licenses depending on the region.